[ad_1]

Please use the menu beneath to navigate to any article part:

Where is the property market now?

What’s driving poor affordability?

What’s driving poor affordability?

How large is the danger of economic instability?

What can be done about each points?

And what’s the outlook for dwelling costs?

These and different questions have been raised and answered by Dr. Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP in his latest Insight.

For so long as I can recall housing affordability has been a problem in Australia however because the Nineties it’s gone from being a periodic cyclical concern to a persistent downside.

The 20% rise in costs over the past 12 months has put the highlight on the difficulty once more.

With the surge in home costs because the Nineties has come a surge in debt which brings with it the danger of economic instability ought to one thing go fallacious within the capacity of debtors to service that debt?

Home costs up 20% in a 12 months

After a dip across the mid-last 12 months in response to the preliminary nationwide coronavirus lockdown, common residential property costs have since risen round 20% in accordance to CoreLogic.

The good points have been led by homes and regional Australia, with models and Melbourne lagging.

And whereas the month-to-month tempo of development has slowed from 2.8% in March, regardless of east coast lockdowns day by day CoreLogic knowledge signifies that it remained robust at round 1.3% in September.

The good points have been pushed by record-low mortgage charges, purchaser incentives, a decent jobs market, a need for extra dwelling house on account of the pandemic and working from dwelling, quite a few authorities dwelling purchaser incentives, the “fear of missing out” and decrease than regular listings.

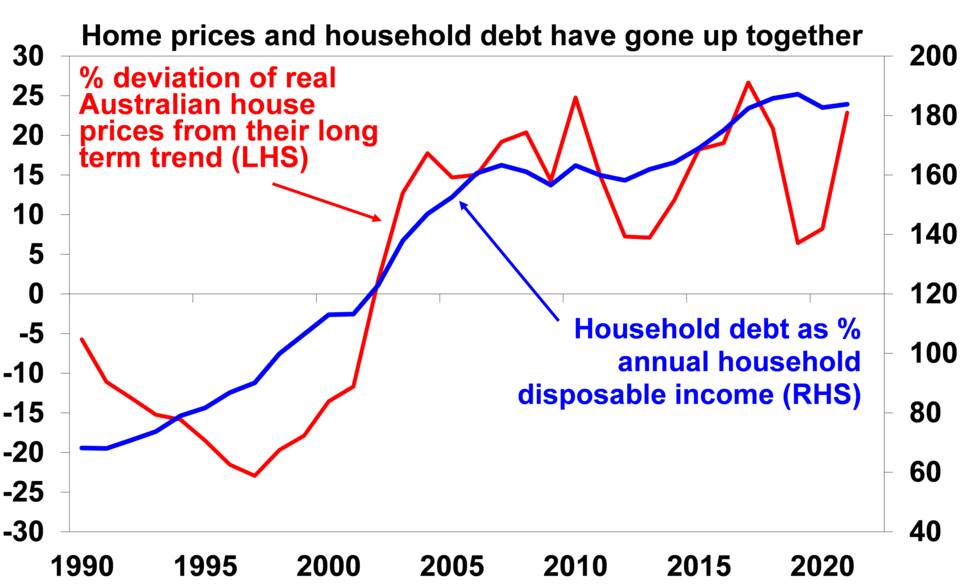

This has pushed common costs to report highs & actual home costs to round 23% above their long-term pattern.

Poor affordability

As can be seen within the final chart home costs have been effectively above pattern for practically the final twenty years.

This brings us to the difficulty of chronically poor housing affordability.

Over the final 20 years, common capital metropolis dwelling costs rose 200% in contrast to an 82% rise in wages.

Over the final 10 years, dwelling costs went up 58% & wages by solely 26%.

The ratio of common home costs to common family disposable earnings has greater than doubled over the past thirty years from round 3 instances to round 6.5 instances.

Affordability has deteriorated extra in Australia than in different comparable nations.

According to the 2021 Demographia Housing Affordability Survey, the median a number of of home costs to earnings for main cities is 7.7 instances in Australia in contrast to 4.8 instances within the UK and 4.2 instances within the US. In Sydney, it’s 11.8 instances and in Melbourne, it’s 9.7 instances.

The ratios of home costs to incomes and rents versus long-term averages are on the excessive finish of OECD nations.

While rates of interest might be at report lows, the surge in costs relative to incomes has seen the ratio of family debt to earnings rise practically 3-fold over the past 30 years, going from the low finish of OECD nations to the excessive finish.

While rates of interest might be at report lows, the surge in costs relative to incomes has seen the ratio of family debt to earnings rise practically 3-fold over the past 30 years, going from the low finish of OECD nations to the excessive finish.

This is making it far more durable for first dwelling consumers to get into the market – it now takes 8 years to save for a deposit in Sydney and practically 7 years in Melbourne.

While authorities grants and deposit schemes can assist pace this up the upper debt burden will take right this moment’s debtors far longer to pay down than was the case a technology in the past.

What’s the issue with excessive dwelling costs?

While a step by step rising degree of dwelling costs consistent with development within the economic system is wholesome and optimistic for the wealth of current property house owners very excessive home costs and debt ranges relative to wages pose two key issues.

First excessive debt ranges pose the danger of economic instability ought to one thing make it more durable to service loans.

Secondly, the deterioration in affordability is leading to rising wealth inequality, a deterioration in intergenerational fairness (as boomers and Gen Xers profit and millennials and Gen Z miss out), confining extra to renting will exacerbate wealth inequality and it is seemingly contributing to rising homelessness.

All of which danger rising the US-style social tensions and polarisation.

READ MORE: Believe it or not, housing affordability has improved

What’s the danger of a monetary disaster?

Predictions that top debt ranges would lead to a crash in property costs threatening the monetary system and the economic system have been a dime a dozen over the past twenty years.

None have come to cross.

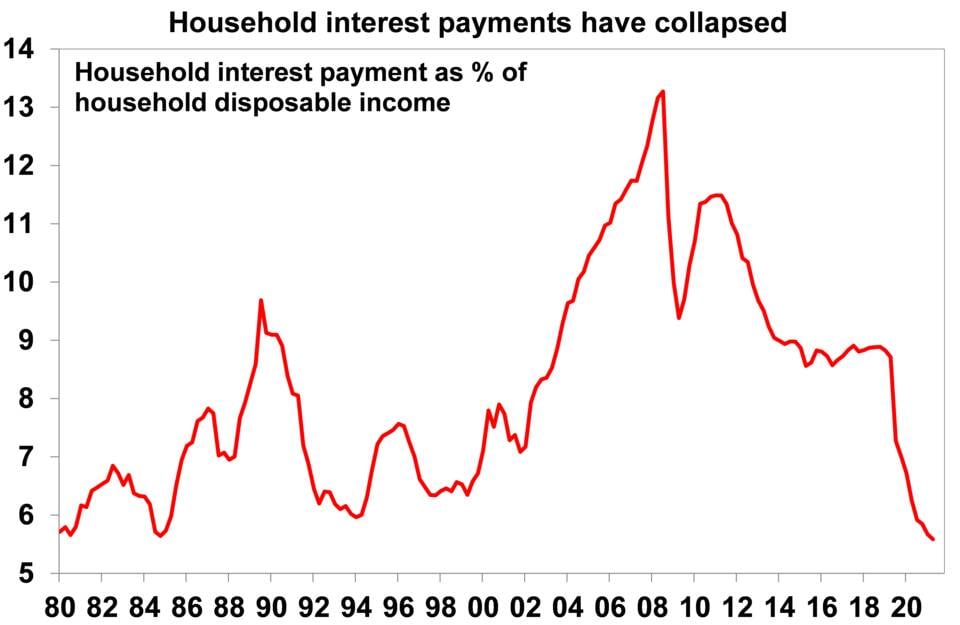

Most debtors are ready to service their mortgages.

Non-performing loans are low & the collapse in mortgage charges has seen family curiosity funds as a share of earnings fall to ranges final seen within the mid-Nineteen Eighties.

However, there is a hazard of getting too complacent right here.

Household debt to earnings ratios are very excessive and permitting them to get ever greater runs the danger that there might be a significant downside sooner or later so it is smart to act pre-emptively to cool issues down.

But whether or not there is the danger of a monetary disaster or not the actually large downside is poor affordability.

So why is housing so expensive?

There are two major drivers of the surge in Australian dwelling costs relative to incomes over the past twenty years.

There are two major drivers of the surge in Australian dwelling costs relative to incomes over the past twenty years.

First, the shift from excessive to low-interest charges has boosted borrowing capacity and therefore shopping for energy.

Second, there was an insufficient provide response to demand.

Starting within the mid-2000’s annual inhabitants development surged by round 150,000 individuals each year and this was not matched by a commensurate enhance within the provide of dwellings leading to a persistent scarcity (see the inexperienced line within the subsequent chart).

The provide shortfall relative to population-driven underlying demand is seemingly the foremost think about explaining why Australian housing is expensive in contrast to many different nations which have low and even decrease rates of interest.

And the focus of Australians in only a handful of coastal cities has not helped both.

A variety of different components have performed a job together with negative gearing and the capital gains tax low cost for traders, overseas shopping for, and SMSF shopping for, however they’ve been comparatively minor in contrast to the persistent undersupply.

And investor and overseas demand haven’t been drivers of the newest surge.

So what can be done?

The excellent news is that we might be getting nearer to the top of the 25-year bull market at property costs: rates of interest are seemingly at or shut to the underside so the tailwind from falling rates of interest is fading; robust dwelling constructing lately and the collapse in immigration might lead to an oversupply of property, and the do business from home phenomenon might take the stress of capital metropolis costs.

However, there aren’t any ensures.

However, there aren’t any ensures.

And issues might simply bounce again on the demand facet as soon as the pandemic recedes and immigrants return.

So a long-term multifaceted answer is referred to as for.

The very first thing to do is to tighten macro-prudential controls to gradual report ranges of housing finance.

Raising rates of interest is not attainable given the weak point and uncertainty hanging over the remainder of the economic system and crashing the economic system to get extra reasonably priced housing will assist nobody.

So, a tightening in macroprudential controls to gradual lending is warranted.

With housing credit score now rising quicker than incomes and at a quicker month-to-month tempo than when APRA final began macro-prudential controls in 2014 and greater than 20% of latest loans going to debtors with debt-to-income ratios above 6 instances up from 14% two years in the past they’re arguably overdue.

This time round traders are taking part in a lesser function within the property growth so macro-prudential controls ought to be broader than was the case in 2014-17.

The major choices are restrictions on how a lot banks can lend to debtors with excessive debt to earnings ratios & excessive mortgage to valuation ratios and elevated rate of interest servicing buffers.

Ideally, first dwelling consumers will want some kind of exemption.

Ideally, first dwelling consumers will want some kind of exemption.

With the Treasurer supporting motion and the Council of Financial Regulators (RBA, APRA & ASIC) expressing concern about family leverage they give the impression of being to be on the best way, though their implementation nonetheless appears a number of months away.

And final decade’s expertise confirmed that they work.

Of course, this is only a cyclical response and extra elementary insurance policies are wanted to deal with poor housing affordability.

Ideally, these ought to contain a multi-year plan involving state and federal governments.

My procuring record on this entrance embrace:

- Measures to increase new provide – stress-free land-use guidelines, releasing land quicker, and dashing up approval processes.

- Matching the extent of immigration in a post-pandemic world to the flexibility of the property market to provide housing.

- Encouraging better decentralisation to regional Australia – the do business from home phenomenon exhibits this is attainable however it ought to be helped together with acceptable infrastructure and after all measures to increase regional housing provide.

- Tax reform together with changing stamp duty with land tax (to make it simpler for empty nesters to downsize) and decreasing the capital gains tax low cost (to take away a distortion in favour of hypothesis).

Policies which might be much less seemingly to be profitable embrace grants and concessions for first dwelling consumers (as they simply add to greater costs) and abolishing negative gearing would simply inject one other distortion within the tax system and might adversely have an effect on provide (though I can see a case to cap extreme advantages).

What is the outlook for dwelling costs?

National dwelling worth development this 12 months is seemingly to be round 20% with costs already up by round 17%. 2022 is seemingly to see property worth development gradual to round 7% on account of worsening affordability, decreased incentives, presumably greater mounted mortgage charges, persevering with decrease than regular immigration & macro-prudential tightening.

If the latter doesn’t occur then we’re seemingly to have to revise up our home worth forecasts.

Guest Author: Dr. Shane Oliver is Head of Investment Strategy and Chief Economist at AMP Capital. You can learn the unique article here.

READ MORE: 20-year analysis shows housing affordability continues to decline but rental affordability is stable

[ad_2]

Source link