[ad_1]

Wondering what’s happening in our rental markets?

Let’s start with some helicopter numbers.

Table 1 outlines the current housing rental vacancy rates across the larger urban areas in Australia.

Most locations have a vacancy rate under 1%.

Weekly rents for detached houses have risen by 15% over the last twelve months.

Weekly rents for detached houses have risen by 15% over the last twelve months.

It now costs, on average, $570 per week or $30,000 per year to rent a modest three-bedroom detached house in Australia.

And whilst not included in the table, median weekly rents for two typical two-bedroom apartments have risen by 12% since this time last year.

That median rent is $425 per week or $22,000 per annum.

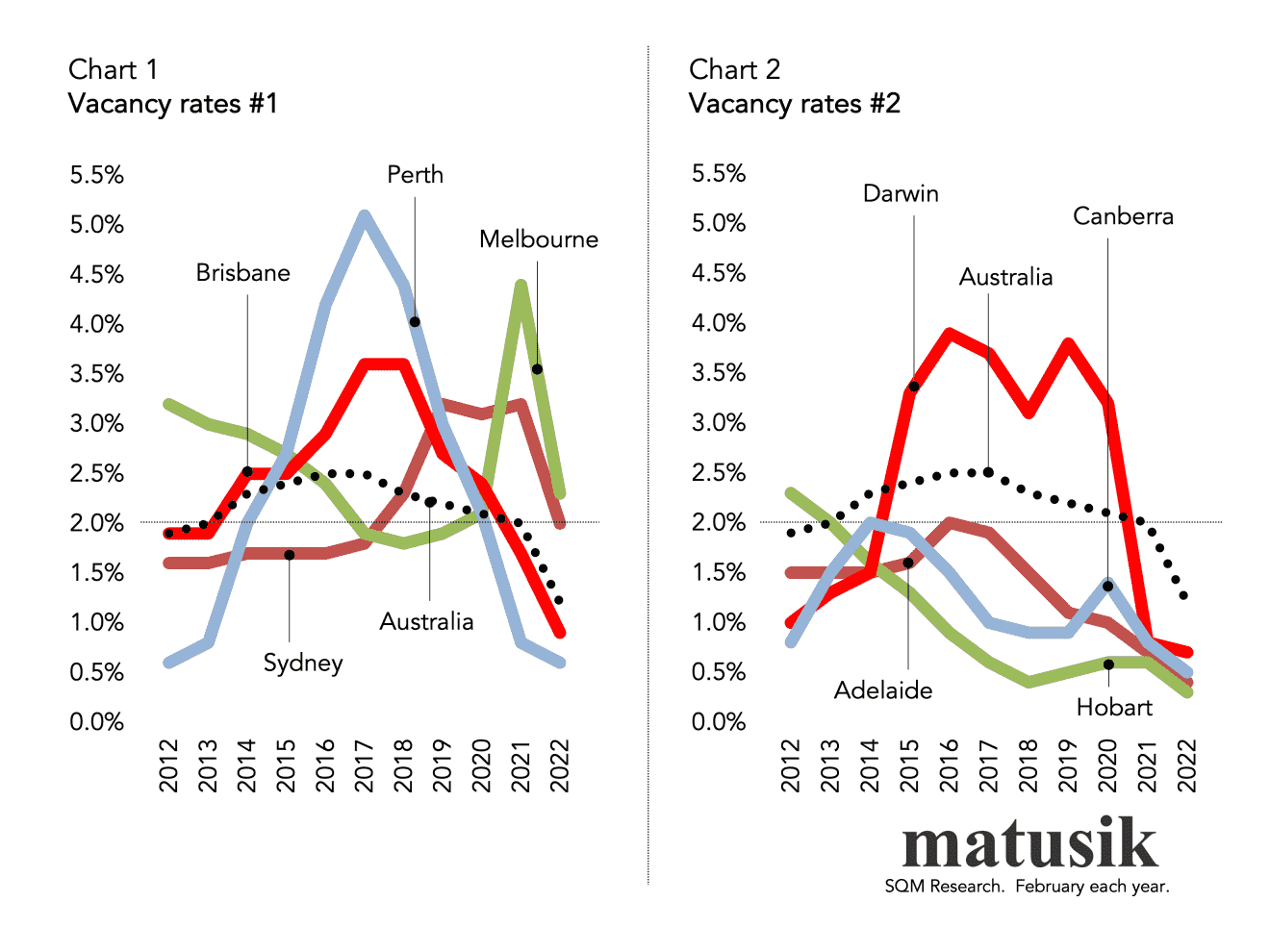

Charts 1 and 2 illustrate the vacancy rates of each capital city over the past ten years.

Each location has its own cycle, but they have all now synced up.

Weekly rents are very much influenced by rental supply.

My experience is that rents rarely fall unless the vacancy rate heads towards 3% and stays elevated for longer than a year, but they show little growth until the vacancy rate falls below 2%.

Every market I have studied shows a similar trend.

The often-used 3% vacancy rate – as a measure of rental balance – did apply when communication was based largely on paper and tenants used to get a “For Rent” list from the local real estate agent and were shown available properties on a weekend.

I am old enough to have experienced such things.

In more recent times, of course, everything is digital – except the actual inspections and sadly often the tenant approval part – so the rental market acts much more quickly when rental vacancies appear, hence a tighter 2% vacancy rate is a more appropriate measure of balance these days.

Chart 3 exemplifies this trend.

There is a debate at present about why the vacancy rate has fallen so sharply in recent years.

This is especially the case given that Australia’s population growth slowed rapidly due to Covid-related immigration restrictions and HomeBuilder (plus record low interest rates) boosted new housing approvals.

This is especially the case given that Australia’s population growth slowed rapidly due to Covid-related immigration restrictions and HomeBuilder (plus record low interest rates) boosted new housing approvals.

Some have been citing a fall in rental household size, others the rental Covid-related Eviction Moratorium (now expired) and/or a change in landlord mindset, with some investors opting to keep their assets empty and rest on capital gain and foregoing a yield.

Net rental yields are often low and with record price growth over the last two years, there might have been some landlords that have gone done the ‘locked-up’ route.

But the main reason for the synced fall in vacancy rates in recent years has been the big fall in the number of housing investors across Australia.

This fall in investor activity was principally due to APRA placing a brake on the proportion of investment loans.

This fall in investor activity was principally due to APRA placing a brake on the proportion of investment loans.

A 10% annual growth benchmark on investment loan growth was introduced in 2014 as part of a range of actions to reduce higher-risk lending and improve banking practices.

This was removed in 2019.

But the consequences of this policy can be felt today and the relationship between investing lending and the rental vacancy rate is shown in chart 4.

New Construction

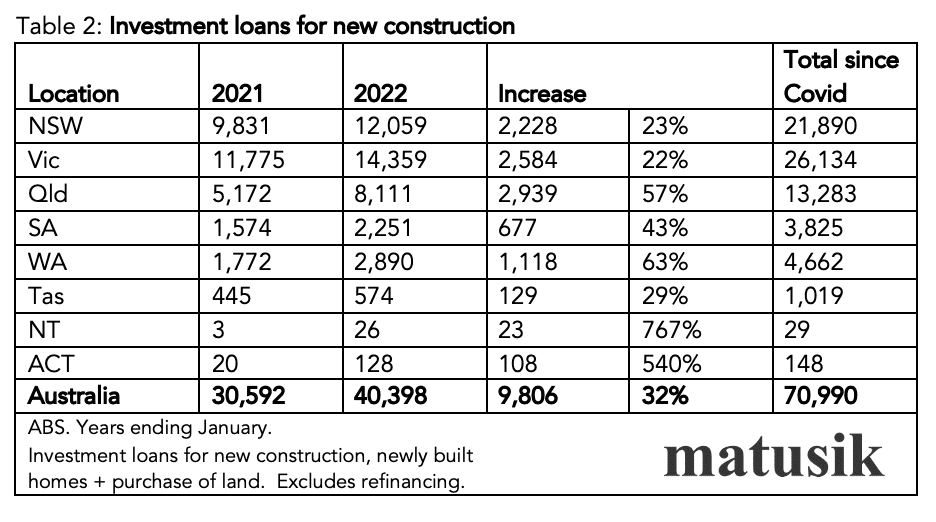

My final table shows that there were just 40,500 new construction-related investment loans approved across Australia over the last year.

This is up 32%, or by around 10,000 new housing investment loans, over the last twelve months.

And since February 2020, some 71,000 new construction-related housing investment loans have been approved across the country.

Assuming that about 60,000 or 85% of these potential new rental properties are built and tenanted out (past trends suggest that this is the likely result), then this will see the size of Australia’s rental market lift by just 1.5% to just over 3.7 million properties.

Assuming that about 60,000 or 85% of these potential new rental properties are built and tenanted out (past trends suggest that this is the likely result), then this will see the size of Australia’s rental market lift by just 1.5% to just over 3.7 million properties.

My back-of-the-envelope calculations – assuming a return to the 400,000 annual increase in Australia’s population growth (150,000 from natural increase and 250,000 from net overseas migration) – see the need to build between 55,000 and 60,000 new rental properties per year to cater for this demand.

So, in short, the recent lift in investment lending will do little to alleviate the rental undersupply.

Even if the federal government decides to cap immigration, we still aren’t building enough rental properties.

And yes, Build to Rent is on the rise – but even if all current 40 BTR projects with some 15,630 apartments under construction across the country are completed in the next two years – they will only have a limited impact.

And yes, Build to Rent is on the rise – but even if all current 40 BTR projects with some 15,630 apartments under construction across the country are completed in the next two years – they will only have a limited impact.

Also of note is that some 10,000 or 70% of these BTR apartments are located in Melbourne.

So, the BTR rental supply – to date – is somewhat concentrated.

By contrast, some 160,000 new loans were given to investors over the last twelve months to buy an established investment property.

This number lifts to 250,000 such loans since the start of the pandemic.

The number of investment loans for established properties is currently four times the volume of investment loans for new construction.

More has to be done to increase the supply of new rental property.

Spreading more BTR to other locations and also BTR encompassing other housing stock, such as townhouses and even small-lot detached housing, offers a longer-term answer to insufficient rental supply.

As does the state/territory and even local governments building more rental housing.

This is a lot easier than many pundits think, especially when the government body already owns the land.

[ad_2]

Source link