[ad_1]

Despite the challenges of 2021, the Victorian land market has remained resilient, with sales peaking at record highs.

Despite the challenges of 2021, the Victorian land market has remained resilient, with sales peaking at record highs amid limited stock, while prices have remained buoyant despite the emergence of affordability constraints.

Buyers are still confident about the future as interstate and international border restrictions lift.

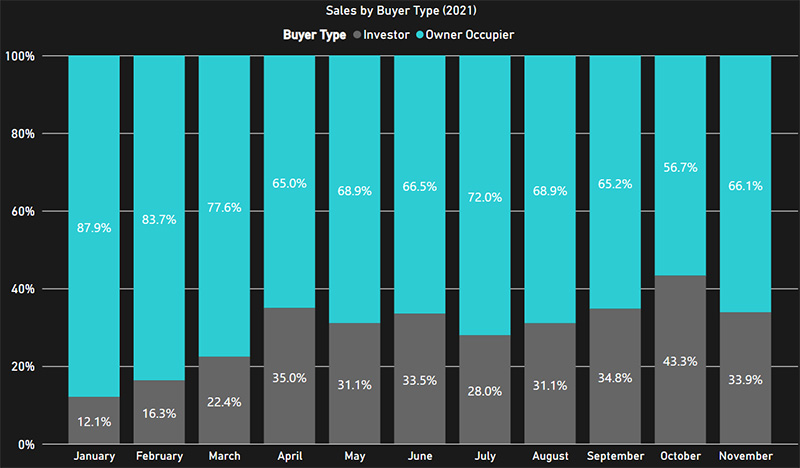

Julian Coppini, CEO of project marketing at Oliver Hume, said enquiries remained high with investors being an increasingly important segment of land sale transactions. Investor demand was underpinned by record low interest rates, increased confidence and expectations around future price growth.

Source: Oliver Hume research January 2021 – November 2021

The Victorian greenfield market is gearing up for a positive 2022 too and will continue to provide opportunities to buyers looking to secure affordable property. With residential property market prices reached new records in 2021 having a knock-on effect on the local greenfield markets seeing new price peaks.

The affordability factor in greenfield markets across metropolitan Melbourne and regional Victoria is the driving force for a healthy interest from buyers in 2022.

Oliver Hume’s National Head of Research, George Bougias, said metropolitan and regional growth area markets, where prices remain well-below the Melbourne average, would continue to attract those looking to enter the market and existing owner-occupiers looking to either upgrade or downgrade.

“With Melbourne’s median house price now above $1 million – and affordability increasingly important – we continue to see growing interest in both metropolitan and regional greenfield land markets in key local government areas (LGAs),”

“The Mitchell Shire is one of the most affordable municipalities and has several advantages, including easy access to Melbourne’s northern region and median land prices are just over $300,000.

“Melbourne’s northern (Hume and Whittlesea LGAs) and western (Wyndham and Melton LGAs) growth corridors saw robust price growth over the year (to the three months ending November 2021), however, median prices remain well-below $350,000.

“Although prices are higher in the south-east growth corridor municipalities of Casey and Cardinia, these markets are also expected to see demand from a range of buyers.” Mr Bougias said.

Median Greenfield Lot Price ($)

| Municipality | Nov-Sep* 2021 | Q-o-Q Aug-Jun** 2021 |

Y-o-Y Nov-Sep* 2021 |

Q-o-Q Aug-Jun** 2021 |

Y-o-Y Nov-Sep* 2021 |

|---|---|---|---|---|---|

| Cardinia | $395,000 | 10.0% | 13.2% | $36,000 | $46,000 |

| Casey | $412,000 | -0.5% | 18.9% | -$2,000 | $65,500 |

| Geelong | $334,000 | 11.0% | 21.9% | $33,200 | $60,000 |

| Hume | $337,000 | 4.3% | 7.3% | $14,000 | $23,000 |

| Melton | $342,500 | 2.5% | 13.8% | $8,500 | $41,500 |

| Mitchell | $304,750 | 10.4% | 19.5% | $28,750 | $49,750 |

| Whittlesea | $339,500 | 3.2% | 11.3% | $10,500 | $34,500 |

| Wyndham | $322,500 | 3.7% | 3.7% | $11,600 | $11,500 |

| Metro Melbourne (Conventional) | $350,000 | 7.7% | 11.3% | $25,050 | $35,500 |

| Metro Melbourne (All Lots) | $349,000 | 7.4% | 10.7% | $24,000 | $33,800 |

| Median (All of Victoria) | $343,000 | 9.2% | 12.5% | $29,000 | $38,000 |

Source: Oliver Hume. *Quarter ending November. *Quarter ending August*.

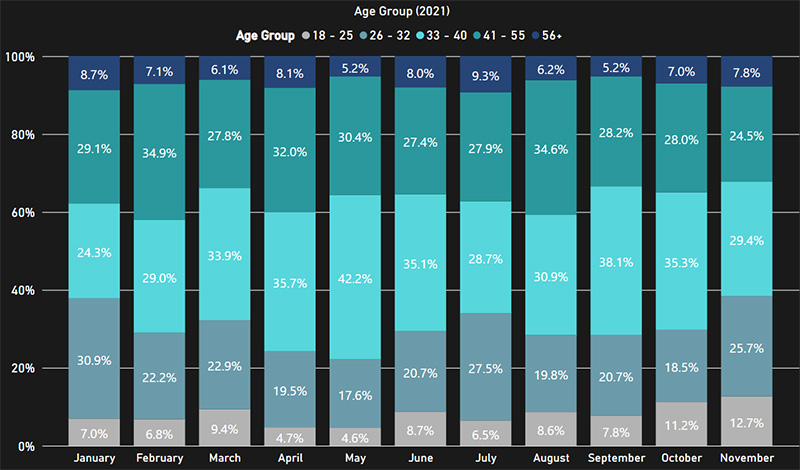

Based on Oliver Hume research, buyers aged 33-40 still remain the key greenfield buyer, but it should be noted that this age segment includes upgraders and investor purchasers as well as first home buyers purchasing later in life.

Source: Oliver Hume research January 2021 – November 2021

“These buyers include, especially, existing owner-occupiers in Melbourne’s south-east and eastern regions who have enjoyed healthy capital gains and are looking to utilise their equity.”

With borders opening and international travel resuming we should see increased migration, population growth, and an improved labour market and consequently a stronger outlook towards economic recovery and a greater pool of potential buyers.

However we may start to see pricing and volumes being impacted by affordability constraints and tighter credit conditions.

“The broader slowdown in the general residential property market is likely to play a role and we have seen price growth moderating in recent months and more listings coming to the market.

“Nevertheless, markets around Australia each have their own unique opportunities and factors driving the next phase of the cycle,” Mr Bougias said.

“Melbourne’s outlook is underpinned by the city’s recovery from extended lockdowns and the opening of the economy, although online platforms remain important, and with COVID-19 seeing widespread adoption of technology, buyers are able to inspect properties after many months of lockdowns.”

Mr Bougias said the outlook for many other key greenfield markets nationally is also positive, with a range of trends expected to shape 2022.

“Southeast Queensland will continue to welcome many more interstate migrants, continuing trends observed before COVID-19,” he said.

“Markets in regional areas and smaller capital cities, for example Adelaide, are arguably at the beginning of a new phase of their growth, with many potential buyers increasingly aware of their outstanding lifestyle and value propositions.”

[ad_2]

Source link