[ad_1]

Well … Sydney finished up the second strongest performing Australian housing market in 2021 with many locations experiencing 25+% house price growth.

Of course, the Sydney property market has been one of the strongest and most consistent performers over the last four decades.

However there is still plenty of growth left, but the rate of price growth is now slowing with a flood of new property listing now hitting the market giving buyers more choice.

Having said that, there are still not enough good properties for sale to meet the extremely strong demand for houses in Sydney, particularly in the inner and middle-ring more affluent suburbs.

Yet the surge in supply of properties for sale gave buyers more choice and took a further edge off auction clearance rates and house price growth as the year came to and end.

Well located, family-friendly apartments in Sydney’s inner suburbs are likely to continue to perform strongly due to increasing demand from owner-occupiers and investors, however apartments in high-rise towers will continue to languish.

Real estate in Sydney’s larger regional locations, and in particular in lifestyle locations like Byron Bay, the Central Coast, the Hunter Valley, Wollongong, New South Wales south coast should also continue to perform strongly with beachside suburbs likely to outperform the wider overall market,

More investors are getting into the Sydney market now recognising that there are no bargains to be found, but that in 12 months time the properties they purchase today will look like a bargain.

Sydney’s new listings lifted strongly as the spring selling season got underway.

The strength of the Sydney property market is also highlighted by the consistently strong auction clearance rates exhibited every weekend this year.

At the same time rents have risen for Sydney houses in particular but rents are still flat in Sydney’s high rise apartment market segment.

Now I know some potential buyers are asking “How long can this last? Will the Sydney property market crash in 2022?”

They must be listening to those perma bears who have been telling anyone who is prepared to listen that the property markets are going to crash, but they have said the same year after year and have been wrong in the past and I will be wrong again this time.

Recently both all our major banks have updated their property price forecasts in response to the market’s resilience in the face of extended lockdowns.

Of course, over the past year, Australia’s property market values have increased at rates not seen in over a decade, and Sydney has led the charge.

This has been good news for homeowners but heartbreaking for house hunters.

At the same time, there have been mixed messages in the media about what’s ahead.

There’s always the Negative Nellies wanting to tell anyone who is prepared to listen to them the market is about to crash, but other more solid commentators are suggesting our property market is slowing down.

And I agree, I believe the pace of capital gains has peaked, but I’m not suggesting home values are about to dip, far from it.

Rather I believe we’ve moved from a peak rate of growth to a pace of capital gain that will be more sustainable and there’s plenty of life left in the Sydney real estate market with property values likely to keep increasing throughout 2022 and into 2023.

Australia’s economy seemed like it was going to experience that V shape recovery everybody had been was hoping for, but that was put on hold by the lockdowns in Sydney caused by the resurgence of coronavirus, but now that this is coming under control we’re likely to see strong economic growth and employment growth and this financial security will underpin Sydney property market moving forward.

When the international borders eventually open Sydney will be a favourite destination for students and highly skilled workers and this will put another “rocket” under the Sydney housing market.

However, some sectors of the Sydney property market will continue to languish.

The sectors of the Sydney real estate market likely to underperform most moving forward will be:

This means that you can’t just buy any property and count on the general Sydney property market to do the heavy lifting over the next few years, so careful property selection will be critical.

To help give you a better understanding of what’s really going on I’m going to explore the nitty-gritty behind Sydney’s market trends, the areas where long-term growth is still likely, and the impact of shifting demographics on the city’s future performance.

I see Sydney’s property market continuing growing at the rate of 6 to 7% per annum throughout 2022 until eventually, affordability slowed the market down.

Remember the current strong upturn phase of the property cycle only commenced in October 2020.

Normally the upturn stage of the property cycle lasts a number of years and is followed by a shorter boom phase which is eventually cut short by the RBA raising interest rates or by APRA introducing macroprudential controls to dampen the exuberance of property investors and home buyers.

However, this time around we have experienced an unprecedented rate of growth seeing our property markets perform even more strongly than anyone ever expected, with the rates of house price growth at levels not seen for a number of decades.

While a lot has been said about the 20% increase in property values many locations have enjoyed so far this year, it must be remembered that the last peak for our property markets was in 2017 and in many locations housing prices remain stagnant over a subsequent couple of years and it was really only early in 2021 that new highs were reached.

This means that average price growth was unexceptional over the long term, averaging out at around 4 per cent per annum over the last 5 years

But recently there seems to have been a change of sentiment about our housing markets from our financial regulators, the banks and even our treasurer.

The Council of Financial Regulators, the club of four main financial watchdogs, showed concern about the increased level of home lending in the first half of the year.

In particular, they signalled their concern about the number of mortgages taken out at more than six times the borrower’s income.

The council has asked APRA to put together a list of potential measures, but this is going to be a challenge and their response will need to be measured so as not to create unintended consequences such as a severe property downturn.

Just look back to 2014 when APRA checked house price growth by targeting investors and restricting the size of what they could borrow relative to the value of their housing collateral.

While tougher lending standards will certainly take some heat out of Australia’s property markets by restricting the number of people that can get home loans, or lessening the amount they can borrow, the move could backfire in the short term as investors and homebuyers try to rush and buy to beat the buzzer on the upcoming tightening of lending conditions.

Back to the question of when will this property cycle end – there is little doubt that Macro-Prudential controls will have a negative impact on our property markets and slow the rate of growth of housing values.

After all, that’s what they’re intended to do.

Whether the markets will just experience slower growth or stop dead in their tracks will depend on what measures are introduced.

Targeting debt to income ratios will have a limited impact on higher wealth households, who often have multiple streams of income.

However, it will affect lower-income households and those purchasing property for the first time.

If you think about it, first home buyers don’t have a “trade-in” of a previous home and therefore need to borrow higher loan to value ratios.

On the one hand, the government says it wants to encourage first home buyers, and on the other hand, it is encouraging the regulators to sideline them.

So in the meantime, it’s just a matter of ‘wait and see’ what our regulators choose to do.

I hope they have learned from the results of previous interventions, otherwise, if history repeats itself, there will be some unintended consequences.

Watch this space.

Let’s start with a bit of history… Sydney property values have grown more than 400% in the past 30 years.

That’s the cost of living in an international city on the water which offers an unparalleled lifestyle.

Unit values continued to decline through to January 2021, as low levels of investor participation, and subdued rental conditions saw less interest in unit stock.

As the Sydney lockdown reinforces the lasting impacts of COVID-19 on large cities, and monetary policy remains accommodative, Sydney-siders who can afford it may still be willing to fork out a premium for detached housing in the months ahead.

Historically, the city’s property market has gone from strength to strength.

Over the last 40 years, Sydney’s average capital growth was 7.4% meaning many properties doubled in value every decade.

And now the Sydney housing market is on the move as can be seen by the rise in asking prices:-

Source: SQM Research

The following chart shows how well Sydney dwelling fared through last year’s CoronaVirus pandemic.

The Sydney Apartment Market

Sydney has embraced apartment living more than any other Australian capital and family suitable apartments are seen as an affordable alternative to houses and units in popular areas such as Sydney’s eastern suburbs and Northern Beaches, where they are likely to enjoy continuing strong demand which will result in a strong increase in values.

On the other hand, apartments in high supply areas present a significant risk to property investors.

This trend already occurred prior to COVID-19 where certain areas in Sydney experienced major unit oversupply.

It seems the property investors are slowly understanding the risks associated with high-rise tower apartments in Sydney including potential construction defects, high vacancy rates, lack of scarcity, lack of capital growth and the challenges of buying in buildings that are predominantly owned by investors, and often many overseas investors.

On the other hand, family-friendly apartments in medium and low rise buildings within Sydney’s inner and middle-ring suburbs are likely to perform well as investments.

With capital growth in houses outperforming apartments so far this year, the pricing gap between houses and apartments is around 50%, so I see increasing demand for these more affordable apartments moving forward.

This will be partly driven by investors returning to the market, so by first home buyers who are being priced out of standalone houses in Sydney.

Prior to Covid-19 metropolitan Sydney required about 41,000 additional dwellings per annum to accommodate its population growth which was underpinned by overseas and interstate migration.

To meet this demand the delivery of new apartment projects was vital, particularly as affordability pressures, demographic trends, changing household types and lifestyle preferences drive the need for more diverse housing options.

And then came CoVid19…

But the new apartment market was already feeling the effects of a downturn in Off-the-Plan (OTP) purchaser demand.

The following graphics from valuers Charter Keck Kramer give a good picture of what’s currently happening in Sydney’s apartment market

The closure of international borders has caused a significant reduction in tenant demand as net overseas migration inflows effectively fell to zero.

So far, the owner-occupier market is holding up, supported by low-interest rates, which have improved affordability for those with jobs.

First, home-buyer demand is being encouraged by stamp duty concessions.

In turn, this is supporting demand for affordable apartments that are suitable for owner-occupiers.

Both upgraders and downsizers remain active where they are transacting within the same market.

Over the last few years, an apartment oversupply and other regulatory and non-regulatory factors have resulted in the collapse of investor demand for Sydney “off the plan” apartments.

The reduced sales volumes have made it more difficult for developers to achieve the pre-sale hurdles required by the banks to finance developments, and a few new projects are on the drawing board.

This means that undersupply of apartments is looming.

But be careful – many of the new Legoland apartment high-rise towers will always remain secondary quality and become the slums of the future – steer clear of these.

The looming undersupply of new projects will lead to lower vacancy rates, rental growth, and eventually, property price growth of these new apartments and in turn, will help fuel increase price growth of well-located establish a purpose in Sydney.

Top 10 Sydney school zones for house price growth

Whether you’re a property buyer or investor, proximity to certain school zones should be a major consideration when buying your next home.

A well-rated school can do wonders for property value, and recent data shows that school catchment zones can actually have a significant influence over how quickly property prices grow.

A well-rated school can do wonders for property value, and recent data shows that school catchment zones can actually have a significant influence over how quickly property prices grow.

In fact, Domain Group’s latest 2021 School Zones Report shows that while Sydney’s property market has been going gangbusters this year, house prices in some of Sydney’s school zones have outperformed and skyrocketed by more than 40 per cent over the past 12 months as fierce competition to get into preferred school catchment areas continues to drive property price growth.

Annual house price growth in 40% of the primary and 41% of secondary school zones analysed surpassed the respective suburb price growth, with almost one-third of school zones seeing up to 10% more growth compared to the suburb they are located in.

House prices in Burraneer Bay Public School catchment zones grew ten times faster than the suburb it is located in (Cronulla).

Proportionately more secondary school catchment zones had positive house price growth and more outpacing the respective suburb house price growth.

House prices have risen across most school catchment zones analysed, with 89% of primary and 95% of secondary schools increasing annually, aligning with the rising property market.

While the top school catchment zones were spread across inner, middle, and outer suburbs, many that topped the list favoured lifestyle locations, spanning coastal suburbs or near to national parks.

House price growth varied between neighbouring school zones. House prices in Balgowlah Heights Public School catchment zone jumped 33% annually, while the neighbouring school zone of Manly West Public School dropped 7.9%.

Domain’s chief of research Nicola Powell said the pandemic had helped supercharge school catchment prices with flexible working allowing young families to relocate to suburbs with easy access to beaches, parks, and schools.

“It’s astonishing to see that starting on a high base of house prices, one-in-10 school catchment zones are achieving 10 to 20 per cent more than the suburb they are located in,” Powell said.

We know that as part of the property decision-making process, parents and investors consider the geographical location of a potential property in relation to a school catchment zone.

When people are looking for a home, they’re looking for a lifestyle, and education is a big part of that picture, be it in the inner-city suburbs or the coastal regions of Australia.”

Dr. Powell explains that the boundary of a public school catchment is often a critical factor when it comes to purchasing a family home.

In Sydney, secondary school catchments appear to have a more positive impact on house price growth compared to primary school catchments.

Which catchment areas come out on top for Sydney?

Here’s the list of the top 10 Sydney high schools catchment areas:

Here’s the list of top 10 Sydney primary school catchment areas:

Sydney’s Rental Market

While over the long term rentals have grown in line with property values, more recently rental growth has slumped, in part due to the influx of rental properties that were previously let on short-term leases such as AirBnB and student accommodation.

As a consequence, overall yields have declined as can be seen from the following chart from SQM Research.

Traditionally in Sydney, vacancy rates have been tight; hovering well below the level of 2.5% vacancies, which traditionally represents a balanced rental market.

However currently the overall vacancy rate in Sydney has crept up to close to 4%, but this varies in different locations.

At Metropole Property Management our vacancy rate is less than half this rate, in part because our clients have chosen investment-grade properties, but we’d like to think it also has a bit to do with our proactive property management policies.

Sydney’s Average Capital Growth

In 1993, the average house price in Sydney was $188,000.

However, dwelling price growth in Sydney has been very fragmented.

While some suburbs has just chugged along others are strongly outperforming.

You see…Sydney is comprised of dozens of smaller markets, each of which has its own drivers and supply/demand issues.

Sydney’s more affluent inner eastern, Lower North Shore, and inner western suburbs have well outperformed these averages.

Houses: In September 2019, only 5% of Sydney suburbs had a median house value lower than $500,000, compared with 22% five years ago.

The proportion of suburbs with a median house value of $1 million or higher was 47% in September 2019, up from 34% five years ago.

Units: 29% of Sydney suburbs recorded a median unit value of $500,000 or less in September 2019, down from 49% five years ago.

The proportion of suburbs with a median value of $1 million or higher jumped from 2.9% five years ago to 14.4% in September 2019.

Overall Sydney is a city in gentrification, with the fingerprints of a younger demographic upping the desirability of the city lifestyle.

Houses and apartments in Sydney’s easter, inner west and lower North Shore suburbs offer the best prospects of long term capital growth as this is where there are more Skill Level 1 worker – those who earn higher incomes, often having multiple sources of income.

Fact is, the rich are getting richer and they are able to and prepared to pay more for their homes

In its relatively short history, Sydney experienced near starvation, rebellion attempts, a gold rush, trade booms, the Great Depression, two world wars, and hosted the Summer Olympics.

6 reasons to choose Sydney

1. Sydney’s demographics

Sydney is Australia’s most populous city and is also the most populous city in Oceania.

ABS statistics showed the population of Greater Sydney, which includes the Blue Mountains and Central Coast, reached 5,005,400 at the end of June 2016 after adding a million people in just 16 years.

That was an increase of almost 83,000 in the previous year, and the city’s fifth-largest annual population increase in absolute terms since 1901 with Sydney absorbing 78 per cent of NSW’s total population increase in 2015-16.

Sydney’s population grew by 1.7 per cent last financial year while the rest of NSW grew by 0.8 per cent giving the State an overall annual population growth of 1.6%.

Of course with our borders currently closed, immigration is going to be virtually non-existent in 2020 and probably in 2021, but once we reopen our borders, it is likely that Australia’s appeal to overseas immigrants is only going to be stronger and Sydney has always been a preferred destination.

Firstly it is an iconic world-class city, but also Sydney offers strong job opportunities.

It took the harbour city almost 30 years, from 1971 to 2000, to grow from 3 million to 4 million people but only half that time to pile on its next million.

This makes Sydney Australia’s only global city and a key city within the Asia-Pacific region.

Today Greater Sydney’s population is estimated to be 5.57 million people.

Interestingly around half of its population were born overseas, making Sydney the world’s most multicultural and ethnically diverse city, with over 250 spoken languages.

In fact, more than 70 percent of the state’s population growth comes from overseas migration.

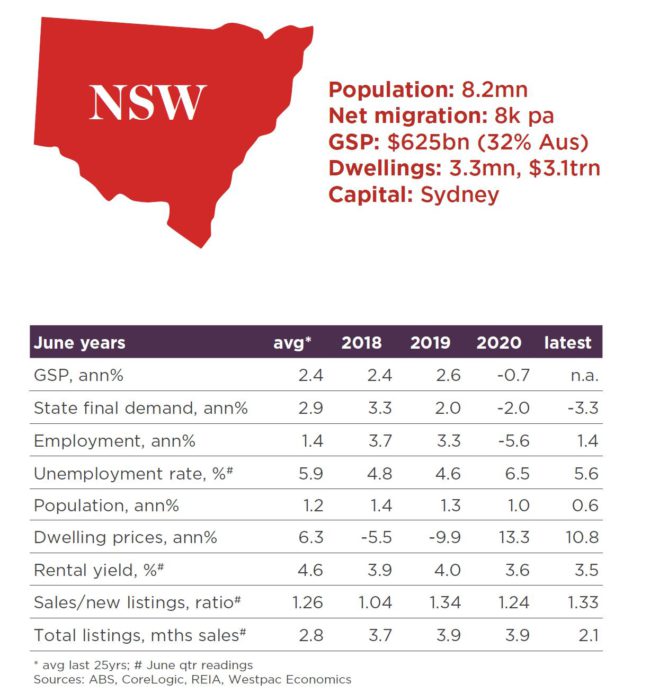

In fact, New South Wales represents around 32% of Australia’s total population.

The median age of Sydney residents was 35 years, and households comprised an average of 2.7 members.

But drilling down deeper, within the CBD, the majority of dwellings are occupied by two adults without children, with the average age of residents reducing to 32.

With distinct areas of trendy, modern districts, Sydney has undergone incredible change since its early days as a settlement city.

Formerly gritty housing zones, originally built for labourers, are being revived and modernised, increasing their allure for those after a modern city lifestyle.

The Rocks is an excellent example of an area going through gentrification, with prime waterfront government housing transitioning to private dwellings.

These types of renewal projects are sure to bring new life – and growth.

Similarly, gentrification is changing the face of Sydney’s Inner West.

Looking back European settlement in Sydney began in 1788, and in 1800 Sydney had around 3,000 inhabitants.

It took time for its population to grow – in 1851 its population was only 39,000, compared with 77,000 in Melbourne.

Sydney overtook Melbourne as Australia’s most populous city in the early twentieth century and reached the million inhabitants milestone around 1925.

The opening of the Sydney Harbour Bridge helped pave the way for further urban development north of Sydney Harbour.

Post-war immigration and a baby boom helped the population reach two million by 1962.

Read more: There’s a 6 month moratorium on evictions – what should I do?

2. Sydney’s layout

One of the largest cities in the world, the metropolitan area has about 650 suburbs that sprawl about 70 km to the west, 40 km to the north, and 60 to the south.

Greater Sydney extends from the coast at the east back to the foothills of the Blue Mountains, with a relatively compact CBD located around i ts famous harbour.

ts famous harbour.

South of the harbour is the desirable inner suburbs and densely populated beaches, including Bondi Beach.

North Sydney, connected to the CBD by the Sydney Harbour Bridge and tunnel, is home to a thriving business district and some of Sydney’s most affluent suburbs, including the Upper and Lower North Shores.

Plans are underway to build a motorway link to open up access between the pricey eastern suburbs and the western district, which makes up the majority of metropolitan Sydney.

Changes in the positioning of major companies to outlying ‘mini-cities’ like Parramatta may see a shift in buyers heading to these cheaper housing areas and employment opportunities.

Developers have anticipated this, but as is often the case, they’ve gone overboard and there is now a significant oversupply of new and off the plan apartments in Parramatta

3. Sydney’s infrastructure

With leading universities, premier shopping districts, iconic landmarks and lively urban flavour, it’s clear why Sydney is considered one of Australia’s most desirable cities to live in.

Built around the world’s largest natural harbour, Sydney offers three efficient modes of transport in, around, and out of the city: road, rail and ferry.

Anyone who lives in Sydney knows all too well that driving more than an hour each way to and from work is the norm.

But this is likely to change with light rail playing an important part in the future of transport in Sydney providing quick transportation around the CBD.

Further construction is underway to connect outlying suburbs to existing rail lines, with plans to extend the light rail system to the Eastern suburbs.

Sydney Airport, the busiest in Australia, handles over 35 million passengers a year, is located only 8km from the city and connects directly to 100 destinations around the world.

Proximity to major highways and rail systems can either boost capital growth or hinder it, and all aspects must be taken into account when considering any property purchase.

4. Sydney’s economy

Largely a manufacturing city in its heyday, Sydney has evolved into a metropolis of high-end, knowledge-based jobs in the business and financial services sector, earning itself the title of Asia-Pacific’s economic hub.

Tourism and hospitality are its next leading employment industry.

Of course, job creation and rising confidence also lead to population growth, which further fuels the property market.

Of course, job creation and rising confidence also lead to population growth, which further fuels the property market.

Inner-city employees earn an average individual wage of $888 per week, compared with $619 for those working in the Greater Sydney area.

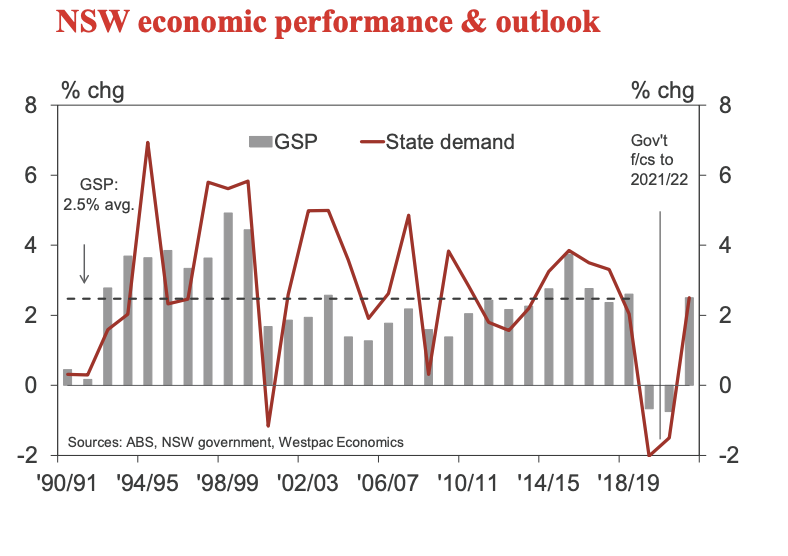

However due to COVID-19 output in the New South Wales economy contracted in the 2019 20 financial year, declining by 0.7%. That was the first contraction in decades, with the state reportedly avoiding the early 1990s recession.

While some headwinds still remain, the state’s economic performance has increased as can be seen in the following chart.

Population growth in New South Wales has come to a standstill as a result of international border closures.

The foreign student sector and international tourism, which are key sectors in New South Wales have been hard-hit.

With the recent boom in property prices, many buyers are finding themselves locked out of the property market, which may signal an increase in long-term rentals.

More than 55% of dwellings in the city are rentals, where occupants – primarily single professionals and couples without children – are willing to pay a premium to live in the heart of the city near to their work and all the action.

Source: Westpac June 1st 2021

5. Sydney’s growth

Since the 1970s, Sydney and Melbourne have been locked in a head-to-head race for the highest population growth, with both cities adding 1.7 million new residents over 40 years.

Overall, Australia’s growth rate is amongst the highest in the world, with the Australian Bureau of Statistics estimating that 66% of residents live in our capital cities.

With an estimated population of 8,046,070 persons, the population has increased by 123,813 persons or 1.6% over the past year, which is in line with the national rate of growth.

The 123,813 person increase was the greatest since September 2017 and was made up of a natural increase of 53,711 persons, net overseas migration of 91,999 persons, and a loss of 21,897 persons due to net interstate migration.

The natural increase of 53,711 persons was the greatest on record while the 91,999 persons increase due to net overseas migration was the largest increase in 12 months.

The loss of 21,897 residents due to net interstate migration was slightly lower than the previous quarter but up from 19,299 persons a year earlier.

The NSW government is planning extensive additions to its transport infrastructure to support future growth, with new motorway extensions providing an uninterrupted connection from Sydney’s south to the north and major road expansions on the plans to ease city congestions.

Outlying suburbs such as Parramatta and Liverpool are developing into regional cities, and with improved infrastructure in the works, there is the likelihood we will see significant population growth in these areas further from the CBD.

6. Sydney’s culture

Sydney is truly a global city, welcoming a broad range of ethnicities from all over the globe.

Sydney is truly a global city, welcoming a broad range of ethnicities from all over the globe.

In fact, nearly half of the people who call Sydney home were born overseas, creating the most dynamic and culturally diverse metropolis in the world.

Each year Sydney celebrates its famous multiculturalism with the month-long Living in Harmony festival, which brings its residents together to celebrate and promote cross-cultural understanding.

Housing in the inner city is attractive to those who love the city life, with tenants looking for properties that include the following features:

- Location – above all.

- Security.

- Storage space.

- Amenity including balconies.

- With street noise generally a given in city living, smart tenants are looking for added features – like double-glazed windows – to minimise the city sounds.

- Cooling – especially over summer

- Technology

- Healthy mobile phone signals

- Great WiFi connectivity.

- Multiple power points

The most prominent Sydney areas

1. Upper North Shore

Statistically one of Sydney’s safest areas, with beautiful parks, large land sizes and an easy train commute to the city, the prestigious suburbs of the Upper North Shore have seen a stable increase in pricing over the years.

Incorporating Pymble, Turramurra, Wahroonga, Warrawee, Killara, Lindfield and Roseville, the Upper North sees a ‘generational’ cycle, with wealthy families moving in to gain access to esteemed private education and excellent public schools. The family moves on once children are out of school, thus allowing the next generations of young families to begin the cycle again.

This trend has maintained steady supply and demand, making the Upper North Shore area one to consider for stable growth, particularly as it sits in the middle ring of the CBD.

2. Lower North Shore

Located just over the Sydney Harbour Bridge and featuring a boon of waterfront properties overlooking the Sydney Harbour, Middle Harbour and Lane Cove River, the Lower North Shore is considered one of Sydney’s most desirable places to live.

While the Upper North Shore attracts families due to the larger land lots and houses, the Lower North has a higher population density with a greater proportion of apartments and units, making it appealing to young professionals who work in the CBD.

The Lower North Shore consists of the suburbs of Mosman, Castle Cove, Cremorne, Neutral Bay, Kirribilli, Milsons Point, McMahons Point, Wollstonecraft, Greenwich, Longueville, Riverview, Linley Point, Lane Cove West, and Chatswood.

3. City and East

Recently positioning itself at 6th on Sydney’s best-performing auction rankings, with a median dwelling value of just over $1 million, the suburbs in East Sydney and the city centre are home to Australia’s highest property earners, including Edgecliff, Rushcutters Bay, Darling Point and Point Piper.

Densely populated and with land at a premium, most properties are small terraced housing or units/apartments, with a higher proportion of renters in the Eastern suburbs than elsewhere in the city.

Suburbs in the city’s inner ring such as Darlington, Chippendale and Darlinghurst have shown interesting changes in their demographic make-up recently, revealing a very high proportion of young, single residents who have populated the area for the social scene and city lifestyle.

Eastern Sydney is also highly desirable, as the home of the famous beachside suburbs of Bondi, Tamarama and Coogee.

While there is no train access to these coastal neighbourhoods, there are strong bus networks.

Read more (and watch the video): How will COVID-19 impact on your banking and loans?

4. Inner West

There is no end of demand from home buyers and investors who want to live in Sydney’s gentrifying inner Western suburbs.

In suburbs like Annandale, Croydon Park, Dulwich Hill, Enmore, Lewisham, Lilyfield, Marrkickville, and Newtown.

The suburbs within the region are characterised by medium to high-density housing and while they’ve been subject to gentrification, this process will continue for decades as the older workers and migrants make room for upwardly mobile high-income earners.

Best advice for new Sydney investors

1. Look for Sydney’s best properties in the inner and middle-ring suburbs

The importance of neighbourhood.

Being locked in a Coronavirus Cocoon has shown us the importance of our neighbourhood.

Social distancing during the COVID-19 pandemic made us experience many painful losses.

Among them were the so-called “third places” – the restaurants, bars, gyms, houses of worship, barbershops, and other places we frequent that are neither work nor home.

If social distancing through coronavirus taught us anything, it taught us the importance of neighbourhood.

If you can walk out of your home and you’re in walking distance of, or a short trip to a great shopping strip, your favourite coffee shop, amenities, the beach, a great park, you will appreciate the benefit of the third-place – the importance of your neighbourhood.

While some people will move to regional Australia to have more space, the majority of Australians will want to continue living in our capital cities, but in lifestyle, destination locations which have great third places.

And it’s likely that in our new “Covid Normal” world, people will love the thought that most of the things needed for a good life could be within a 20-minute public transport trip, bike ride or walk from home.

Things such as shopping, business services, education, community facilities, recreational and sporting resources, and some jobs.

In planning circles, it’s a concept known as the 20-minute neighbourhood, and many inner suburbs of Australia’s capital cities and parts of their middle suburbs already meet a 20-minute neighbourhood test.

However, very few of the outer suburbs would do so and are unlikely to easily do so because it’s about more than walkability.

Tenants, too, will have similar wish lists, and savvy property investors will strive to cater to this.

We know that location will do 80% of the heavy lifting in your property’s performance and that some locations outperform others by 50% to 100% over a decade with regard to capital growth and it’s likely to be those liveable locations that will be highly desired.

A review by the Australian Housing and Urban Research Institute has found that suburbs located within 5 to 15 km of the CBD consistently see a level of capital growth that outperforms suburbs.

These inner and middle-ring suburbs continue to see long-term increases in value because:

Gentrification has changed the look and stigma of ‘ugly duckling’ areas into increasingly attractive places to live.

Sometimes, changes to an area, such as improved road and rail access or a change in demographic, can spur on the gentrification process in a neighbourhood, transforming it into an area that enjoys a steady increase in desirability.

While a rising tide lifts all ships and house prices have risen throughout Sydney, in general, the outer and western suburbs have not had the same level of capital growth as Sydney’s inner and middle-ring suburbs.

2. Steer clear of the new high rise Sydney apartment towers

We’ve seen an oversupply of newly built apartments happen in Sydney.

The problem is not all apartments are the same.

Some will make great investments increased substantially in value over the long term, but many of the high-rise towers built in the last fifteen years will continue to underperform with poor, if any, capital growth in the foreseeable future.

Of course, these Lego Land apartment blocks never made good investments.

They offered little scarcity and had no owner-occupier appeal having been built with investors in mind, and often overseas investors who didn’t fully understand the needs of the local market.

Worse still… because of the high developer margins and marketing costs, many investors paid too much to start with and have since found that on completion their properties were worth considerably less than their contract price.

The sad reality for these investors is that today, in light of the many media reports of structural problems in some of these high rise towers, there is a crisis of confidence with apartment owners concerned about what unknown issues and liabilities may lie ahead for them and potential purchasers are holding back not wanting to buy themselves futures problems.

This sector of the property market has lost the trust of the buying public and confidence will take quite some time to restore as various stakeholders including state and local governments as well as the construction industry including building surveyors and certifiers scramble to shore up the building sector.

You see…there tend to be three major types of building issues faces by apartment owners:

- Structural defects – These are the ones that grab the headlines but, in reality, major structural issues only relate to a small number of buildings.

- Fire issues – These often relate to inferior cladding used during construction. Cladding audits are ongoing, but so far 629 affected buildings have been identified in Victoria alone.

And now it’s been revealed that there’s a list of nearly 450 buildings across the state of NSW with potentially flammable cladding that the State Government is keeping it secret due to security concerns. The list, developed by the cladding task force and provided to State Parliament, was given public interest immunity, which restricts public access.NSW Police Counter Terrorism Command advised the addresses should not be published due to safety concerns. The unit said the information risked prejudicing the interests of building and apartment owners. - Water issues – These are very common and occur to some extent in almost every new building – things like leaking balconies, showers and roofs. While these are a nuisance and can be expensive, they can usually be rectified.

Fact is, the buildings with major problems requiring mass evacuation are the outliers, but for those involved their losses will be significant as they will have hefty repair bills and have no real market for the sale of their apartment in buildings that could well become the slums of the future.

Two tiers of apartments in the future

These issues will lead to a flight to quality, meaning well constructed, medium density apartments and townhouses will continue to be strongly sought after and will keep increasing in value, making them great investments.

At the same time, tighter future construction standards will lead to increased building costs and therefore higher eventual asking prices for the next round of apartments to be built, underpinning the future value of soundly built established apartments.

Similarly, the solidly build older established two and three-story walk-up apartments built in the ’60s and 70’s that used to be called “flats” have stood the test of time and will continue to make good investments.

On the other hand, owners of poorly constructed high-rise apartments in the many “me too” buildings built in the last decade or two will find the value of their properties will languish.

While some of these owners may be keen to cut their losses, they will find their properties difficult to sell and many will not be prepared to or financially able to crystalize their losses, just like many of the unfortunate investors who bought in mining towns during the mining boom are still finding they are stuck with underperforming properties which are worth considerably less today than they paid for them many years ago.

3. Consider making the most of investing in Sydney properties

Sydney properties have exhibited strong capital growth over the long term and are likely to do so in the future.

But with their current low yields comes the challenge of negative gearing.

While this understandably concerns many first-time investors, I see it as a cost of doing business.

Here’s a quick explanation of negative gearing:

A property is negatively geared when the costs of owning it – interest on the loan, bank charges, maintenance, repairs and depreciation – exceed the income it produces.

Since the costs of producing an income are generally deductible against the taxpayer’s other income, property investors can effectively offset some of the interest expense against their wages.

This has made some argue that other, less fortunate, taxpayers help these property investors meet their costs.

Why would you buy a property that makes a loss?

Generally, it’s because property investors hope that their income losses will be more than offset by their capital gains when they eventually refinance or sell their property.

And in Australia capital gain is not taxed unless you sell your property, and then it is concessionally taxed; again evoking the argument that it favours wealthy landlords.

The truth is that negative gearing is more favourable for taxpayers who earn high incomes.

Imagine an investor had excess interest expenses of $10,000.

If they were on a marginal tax rate of 15 cents in the dollar they could use their loss and reduce their tax by $1,500.

But to a taxpayer in a higher tax bracket, one who pays 30 cents in the dollar tax, they could reduce their tax by $3,000.

So the benefits of negative gearing are greater the more you earn and the higher your tax rate.

While negative gearing has its critics, in my mind property investment is about capital growth of your assets rather than cash flow.

Cash flow will keep you in the game, but capital growth will get you out of the rat race.

In the long term, well-located properties in the inner and middle-ring suburbs of Sydney will continue to be highly sought after and keep increasing in value-creating wealth for their owners, be they homeowners or real estate, investors.

And in the current low-interest rate environment, and the Sydney housing market at the lowest they ever have been.

A strategic approach to choosing a strong investment property in Sydney

If I accept that in the short term I’ll be negatively geared, then I must ensure I buy an investment grade property that will outperform the market averages with regards to capital growth, and to do this I use my 6 Stranded Strategic Approach.

- I would only buy a property that would appeal to a wide range of owner-occupiers.

Not that I plan to sell my property, but because owner-occupiers will buy similar properties pushing up local real estate values.

This will be particularly important in the next few years as the percentage of investors in the market is likely to diminish.

- I would buy a property below its intrinsic value – that’s why I avoid new and off the plan properties which come at a premium price.

- In an area that has a long history of strong capital growth and that will continue to outperform the averages because of the demographics in the area.

This will be an area where more owner-occupiers will want to live because of lifestyle choices and one where the locals will be prepared to and can afford to, pay a premium price to live because they have higher disposable incomes.

In general, these are the more affluent inner and middle-ring suburbs of our big capital cities - I would buy a property with a high land to asset ratio.

- I would look for a property with a twist – something unique, or special, different or scarce about the property, and finally

- I would buy a property where I can manufacture capital growth through refurbishment, renovations or redevelopment rather than waiting for the market to deliver me capital growth.

How can I stay on top of current information?

Get property news, updates, and advice by email

There is so much information available about various property investing trends, strategies and market information that it can be overwhelming knowing where (or how) to get started.

Join the 120,000-plus Australians who subscribe to my weekly newsletter, which offers a diverse range of analysis, articles and expert commentary that is essential for successful property investing. Subscribe here now.

Then please subscribe to the Michael Yardney Podcast where twice each week you’ll learn something new about property, success, and money in around 30 minutes.

[ad_2]

Source link