[ad_1]

As Australia’s work practices and buying habits evolve, Australia’s commercial property sector is taking two divergent paths – with profound implications for investors.

As Australia’s work practices and buying habits evolve, Australia’s commercial property sector is taking two divergent paths, with profound implications for investors.

Investors snapped up just shy of $16 billion worth of income-generating industrial and logistics (I & L) assets in Australia in 2021, more than double the previous record.

Through 2021, sales of income-producing assets priced at more than $10 million totalled $15.9 billion in Australia.

That is just over three times the 10-year average annual transaction volume of $4.2 billion, and more than double the previous highwater mark of $7.2 billion set in 2016.

It’s a markedly different scenario for office investment and occupancy.

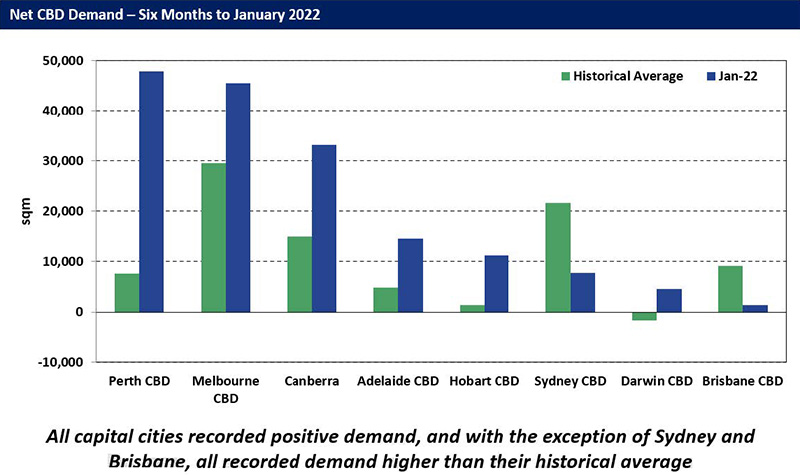

Data from the Property Council’s 2022 office market report shows that Australian office vacancy increased slightly from 11.9 per cent to 12.1 per cent over the six months to January 2022.

A third of the office supply that will become available in 2022 will be in Sydney. While all capital cities recorded positive demand in January 2022, only Brisbane and Sydney were not above historical averages.

Work-from-home arrangements loom as the continued challenge facing office space investors and owners. Even as pandemic-related restrictions ease around the country, office workers are voting with their pyjamas and continuing to work from their own homes.

Brisbane and Melbourne recorded office vacancy increases of 15.4 per cent and 11.9 per cent in January 2022 compared to July 2021, according to the Property Council. Supply also outstripped demand in both cities.

Weaker rents and cash flows will also affect asset values for both office and retail landlords.

“Longer term, consumer preference for online shopping and the prevalence of remote working will remain a key rating focus for retail and office landlords,” the S&P Global Rankings’ report stated.

“However, industries supporting the transition to online shopping are thriving … and industrial landlords are riding the wave of demand for logistics services to support growing online consumption.”

Industrial space scarce, yields rising

Offices around the country were less populated than at any time since the recession of 1993, with the vacancy rate increasing from 11.9 per cent to 12.1 per cent over the six months to January 2022.

It contrasts sharply with industrial and logistics properties, where more floor space than ever before was absorbed but even with the greater supply of sites, demand still managed to drive the national vacancy rate to a new record low of 1.3 per cent.

Through 2021, sales of income-producing assets priced at more than $10 million totalled $15.9 billion in Australia. That is just over three times the 10-year average annual transaction volume of $4.2 billion, and more than double the previous highwater mark, of $7.2 billion set in 2016.

Sass J-Baleh, CBRE’s Head of Industrial and Logistics Research Australia Institutional, said investment appetite continues to favour I&L due to confidence in the ability to collect income.

“Demand from investors and occupiers alike drove Australia’s industrial and logistics sector to new heights in 2021, with records smashed on a host of key metrics,” Ms J-Baleh said.

“Given investment sale transaction volumes had only ever surpassed $5 billion three times before, and peaked at $7.2 billion, the result of $16 billion in 2021 is groundbreaking and demonstrates the strong demand for Australian industrial and logistics assets from local, regional and global investors.”

Australia’s e-commerce penetration rate continuing to rise, now accounting for 14.3 per cent of total spending. This translated into e-commerce entities taking up 19 per cent of space across 2021.

“Lockdowns in the second half of 2021 continued to accelerate the major growth trends for industrial and logistics, as more consumers took their shopping online,” Ms J-Baleh said.

“The transport, postal and warehousing sector finished 2021 as the most-active sector, followed by wholesale and retail traders, that cross-section accounting for 69 per cent of the Q4 leasing activity.”

Average net face rents increased significantly and midpoint yields contracted in each of Australia’s five major cities, with Perth leading the way on both fronts with a 5.6 per cent rental increase year-on-year.

Nationally, super prime average rents grew by 4.4 per cent year-on-year across 2021, prime rents by 7.7 per cent and secondary rents by a record 12.0 per cent.

“We expect rents to grow at an ever-stronger rate in 2022, in excess of 5 per cent year-on-year,” Ms J-Baleh noted.

Investors looking to capitalise on strong occupier demand are increasingly looking to Brisbane’s booming industrial sector.

The city has broken its transaction record for the third consecutive year and is tipped to double its pipeline this year.

Offices on the fringe

Investment does continue to pour into the office property sector, with much of it centred on city fringes and regional centres, rather than the just capital city CBDs.

Property Council NSW executive director Luke Achterstraat said demand for office space had increased in CBDs right across NSW in the past six months, including Sydney, Parramatta, Newcastle and Wollongong.

Investors have followed suit with a record $70.8 billion flooding into commercial real estate, according to the latest Australia Capital Trends report from Real Capital Analytics (RCA).

While industrial and logistics assets were the most keenly sought, office attracted $21 billion from overseas buyers.

Source: Property Council of Australia

Aggregate vacancy levels have risen slightly from 11.9 per cent to 12.1 per cent but the driver of this has been new supply of office space, not a drop in demand, according to Ken Morrison, Chief Executive of the Property Council of Australia.

“The reality is that most CBD businesses continue to see the office as integral their future, and that is reflected in the increased demand for office space over the past six months.”

The office fringe market in Melbourne has risen to prominence on the back of employees seeking more flexible arrangements around returning to the office and employers endeavouring to accommodate that.

“What we have seen is that with people wanting to work from home part of the time and wanting to go to the office but not yet to the CBD until it is safe, companies are looking for fringe suburbs with good public transport and amenities for staff but also easy access to the CBD,” Colliers’ National Director Peter Bremner said.

Fortis Director Charles Mellick said they were also witnessing this suburban surge.

“Over the last few years, we have witnessed the increased demand for premium city-fringe commercial offices in Melbourne.”

The expected end value of Fortis’ Melbourne projects currently under construction or under a planning proposal is $1 billion, with a further $1.25 billion pipeline of work in Sydney.

[ad_2]

Source link