[ad_1]

It is likely that 2021 marked the peak of value growth across Australian dwellings, and may have also marked a peak for sales and listings activity.

Affordability constraints have worsened, vendor activity has surged toward the end of the year, and the housing finance space is currently showing signs of tightening and slowing.

Affordability constraints have worsened, vendor activity has surged toward the end of the year, and the housing finance space is currently showing signs of tightening and slowing.

The accumulated force of these individual headwinds has led many of the major banks to forecast softer growth outcomes for 2022.

Softer growth rates are likely to coincide with fewer purchases, where sales and listings activity eventually move with momentum in price.

The ‘time to buy a dwelling’ component of the Westpac-Melbourne Institute consumer sentiment reading has been softening, averaging 90.4 in the three months to November, down from 94.0 in the three months to August.

Lower growth rates, and the possibility of a decline in dwelling values over the next few years, may also lead to a decline in vendor activity, as the opportune time to sell passes.

Lower growth rates, and the possibility of a decline in dwelling values over the next few years, may also lead to a decline in vendor activity, as the opportune time to sell passes.

However, a slowdown in buyer and seller activity also means a slowdown in debt accrual for Australian households.

This may also mitigate the need for further interventions around risk in housing lending, following the increase to serviceability assessment buffers for borrowers by APRA in October.

Further near-term trends for housing market performance are outlined below.

A continuation of the changing buyer profile

In the three months to October, ABS housing finance data showed total values secured for the purchase of property fell -6.3% compared to the previous quarter, led by a decline in housing finance secured by owner-occupiers (both first home buyers and non-first home buyer owner-occupier finance fell).

First home buyer demand is expected to continue to fall in 2022, having fallen consecutively for the past nine months.

Although in decline, the number of first home buyer loans secured (which was 11,402 through October) remains above the decade average (8,612) but could have further to fall amid deteriorating affordability, and the winding down of first home buyer incentives, which brought forward demand.

This decline could be partially offset by any reactionary government policies in 2022, such as a refresh of federal government home loan guarantee schemes.

First home buyer activity could also steady as property market conditions, such as typical days on the market and new listings, start to shift in favour of buyers.

ABS housing finance data also shows investor activity has been the only source of growth in housing finance over the five months to October.

But even in the investor segment, growth rates are starting to slow.

In the three months to October, growth in secured housing finance for the purchase of investment property rose 4.2%, down from a recent high growth rate of 29.3% in the three months to May 2021.

Notably, international border closures have been accompanied by record-low rates of foreign purchases of Australian real estate, highlighted in the June 2021 quarter NAB Residential Property Survey.

Notably, international border closures have been accompanied by record-low rates of foreign purchases of Australian real estate, highlighted in the June 2021 quarter NAB Residential Property Survey.

NAB reported that the share of foreign buyers in established housing markets hit a record low of 2.0% in the June quarter, and trended slightly higher at 2.2% in the September quarter.

As with domestic housing purchases, more liberated international travel in 2022 and 2023 may see a ‘catch-up’ period of foreign acquisition of Australian real estate, as overseas investors and migrants can visit to inspect the property.

The return of foreign buyers and overseas visitors is likely to see a revitalisation of areas that have been traditionally popular with overseas arrivals, such as the inner-city markets of Sydney and Melbourne.

More ‘affordable’ housing markets to see a temporary boost

Periods of very high growth across desirable housing markets can push demand towards relatively affordable markets.

In the three months to November, this has already become evident across several markets:

- Across Melbourne, outer-suburban areas such as Wyndham and Melton local government areas, among the lowest annual growth rates in dwelling values over the past year, are now among a handful of regions experiencing increased momentum in growth.

- Across Sydney, quarterly growth rates fell from 6.4% in August to 4.3% in November, as the median house value hit almost $1.4 million.

The relatively affordable regional NSW, offering a median house value of around $695,000, has seen quarterly growth rates accelerate to 6.6% in the three months to November, up from 6.5% in the previous quarter. - Across Canberra, quarterly growth rates are seeing an uplift across the unit segment, while growth rates are fading in the detached house segment.

While these more affordable housing markets may see a temporary boost through to the end of the current upswing, the momentum is expected to be temporary, with lower value housing markets expected to follow higher-end markets into a cyclical downturn.

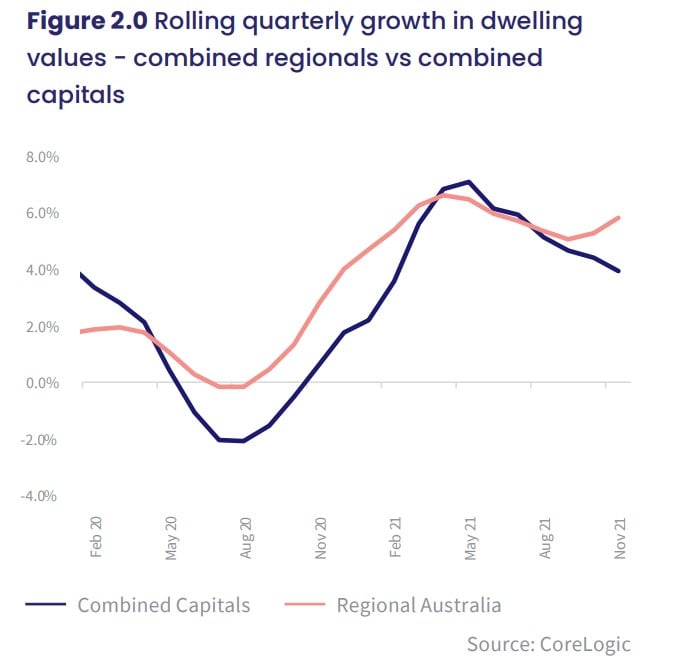

This trend towards regional lifestyle markets is also supported by recent growth trends which have shown a notable divergence in the trajectory of quarterly growth between regional and capital city markets.

A temporary resurgence in regional demand

The beginning of 2022 may be marked by a surge in demand for regional lifestyle markets, similar to the surge which followed the 2020 lockdowns.

The beginning of 2022 may be marked by a surge in demand for regional lifestyle markets, similar to the surge which followed the 2020 lockdowns.

At the end of the extended Melbourne lockdown in 2020, migration patterns across Victoria saw a surge in departures from Melbourne to regional Victoria and Queensland in the fourth quarter of 2020 and the first quarter of 2021.

It is not far-fetched to imagine this being repeated through the end of 2021 and the beginning of 2022, as eased border restrictions make physical inspection and purchase of property easier for those who had been in lockdown across Sydney, Melbourne, and the ACT.

Given the popularity of South East Queensland regions from interstate migrants, the Sunshine State is expected to be a relatively strong performer through 2022.

This trend towards regional lifestyle markets is also supported by recent growth trends which have shown a notable divergence in the trajectory of quarterly growth between regional and capital city markets.

However, there may be forces that offset demand in regional Australia.

For some buyers, housing markets that currently see better buying or renting conditions, such as the inner-city suburbs of Melbourne, may draw demand from those that have been displaced from regional lifestyle markets.

For some buyers, housing markets that currently see better buying or renting conditions, such as the inner-city suburbs of Melbourne, may draw demand from those that have been displaced from regional lifestyle markets.

There may also be some mitigation of remote work trends through vaccine rollouts and return to office initiatives.

The April 2021 edition of ABS Business Conditions and Sentiments survey indicated that while over 40% of Australian firms had embraced some level of remote working since the onset of the pandemic, this is expected to decline long-term.

This may limit the number of feasible relocations from major metropolitan areas over time.

ALSO READ: Here’s what property investors will be doing in 2022

[ad_2]

Source link