[ad_1]

Please use the menu below to navigate to any article section:

For my final blog for 2021, I thought it would be interesting to look back to see how various investment asset classes performed.

This is important for two reasons.

This is important for two reasons.

Firstly, it is wise to benchmark your investment returns so that you can assess relative performance.

Secondly, it serves as a salient reminder about the cost of delay and procrastination.

Short-term returns are unimportant

In isolation, short-term returns are meaningless.

That’s because your focus as an investor must be on maximising medium to long-term investment returns.

What can I invest in today that is likely to generate the highest returns over the next 5 to 10 years?

That is the question you must ask yourself.

Therefore, it’s important to highlight at the beginning of this blog that you should not put too much importance on short-term (i.e. 1 year) investment returns.

Resist the temptation to guess what asset class will perform best next year.

Instead, ask yourself which asset class or investment will produce the highest returns over the next 5+ years i.e. between 2022 and 2027.

It was a year of two halves in share markets this year.

It was a year of two halves in share markets this year.

The first half benefited from strong price appreciation, particularly for value stocks.

The second half was adversely impacted by a few things including the risk that higher inflation may not be transitory, interest rate hikes occurring sooner than expected, central banks tapering Quantitative easing, and more recently, the potential impact of the new Omnicom variant.

The table below sets out returns until the end of November 2021 for the main geographical markets.

Emerging markets predominantly include China, Taiwan, South Korea, and India.

They have been impacted by all the concerns listed above plus many Chinese-specific matters including diplomatic and trade-related tensions, Evergrande default (that occurred last week), tech industry crackdown, and economic growth concerns.

This has conspired to make emerging markets the most attractively priced sub-asset class, behind the UK market, as illustrated in the table below.

Expected returns are calculated by Research Affiliates, LLC using various evidence-based valuation models.

The total return is the aggregate of income + earnings growth + change in valuation multiples.

Bond markets

Australian bond investment returns this year are the worst since 1994.

The Bloomberg AusBond Composite 0+ Yr Index lost 3.23% in the 12 months to the end of November 2021.

Australian corporate bonds have performed slightly better losing circa 2% over the same period.

Global bonds have also produced negative returns over the past 12 months – the Bloomberg Global Treasury Scaled Index (hedged) lost circa 1.5%.

Bond values have been adversely impacted because the market has factored in the risk that interest rates may rise sooner than originally anticipated due to inflationary pressures.

This is a lot more likely in the US than it is in Australia.

Comparatively, it appears that the Australian bond market has overreacted to this risk.

Comparatively, it appears that the Australian bond market has overreacted to this risk.

I should highlight that bonds play an important role in a portfolio’s asset allocation because they are negatively correlated with shares.

That means when shares rise in value, bonds tend to fall and vice versa.

Given share markets are trading close to all-time highs, arguably maintaining bond exposure is even more important today.

Global property and infrastructure

Global property and infrastructure investments are regarded as defensive investments (i.e. safer) because they tend to have long-term contracted revenue, so their future cash flows are more certain.

The global property includes real estate assets such as shopping centres, industrial properties, offices, resorts, and so forth.

Infrastructure includes assets such as utilities (water, gas, electric), toll roads, pipelines, and other large, capital-intensive projects.

Returns for these two asset classes to the end of November 2021 are set out below.

Three issues have impacted returns over the past 12 months.

Firstly, Covid lockdowns are adverse events because they reduce traffic and therefore revenue.

Secondly, low-interest rates positively impact these investments as these products tend to rely on debt funding.

Thirdly, government fiscal policy throughout Covid tends to be focused on increasing infrastructure spending.

The 12-month returns reflect the fact that these asset classes fell substantially between February and October 2020, due to Covid.

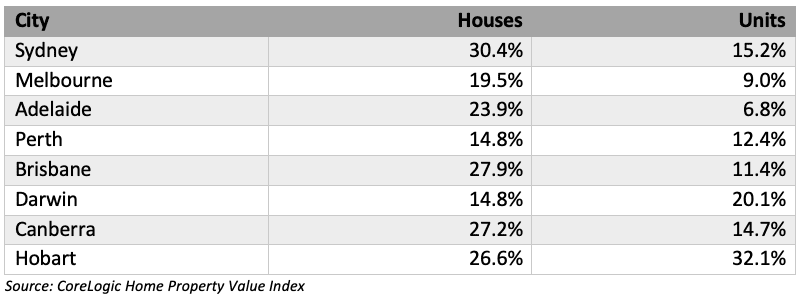

Direct residential property

I probably don’t need to spend too much time discussing the residential property market considering I write regularly about this market in this blog throughout the year.

I probably don’t need to spend too much time discussing the residential property market considering I write regularly about this market in this blog throughout the year.

The table below sets out price changes in each capital city to the end of November 2021.

Whilst growth over the past 12 months has been substantially higher than average, it is important to note that growth over the past 5 years has been below trend as discussed here and that it appears the rate of price growth has normalised in recent months.

Direct commercial property

Some of our clients invest in direct commercial property, as advised by us.

As a rule, we tend to avoid investing in retail commercial property, due to well-documented profit margin pressures that most retail businesses have endured, particularly over the past 10 years.

As a rule, we tend to avoid investing in retail commercial property, due to well-documented profit margin pressures that most retail businesses have endured, particularly over the past 10 years.

Whilst rental yields for industrial property are attractive, they tend to have a single-tenant profile which we don’t feel is appropriate.

As such, we deem the most appropriate sector to be the commercial office.

Given Covid lockdowns and greater adoption of working-from-home, you may assume that the commercial office market has been adversely impacted.

However, that is not the case.

There is a lot of demand for high-quality commercial office buildings, and they have continued to sell for record amounts.

There are two reasons for this.

Firstly, low-interest rates have inflated asset prices.

Firstly, low-interest rates have inflated asset prices.

Secondly, wealthy investors can look beyond the work-from-home rhetoric and see long-term value.

Of course, some segments will perform better than others, and a building’s attributes and location matter the most, but overall, we are very optimistic about future returns in this market, particularly with our evidence-based methodology.

What will you do differently in 2022?

Did you make any investment mistakes during 2021?

If so, what can you do in 2022 and beyond do so that you don’t repeat these mistakes?

You would generally be well-served by adopting this 3-step approach:

Only adopt evidence-based methodologies.

Only adopt evidence-based methodologies.- Focus on a time horizon of 5 to 10 years.

Ask yourself, what will matter in 5 years from now?

Will Covid matter?

Probably not.

Interest rates?

Maybe, but they have probably already been factored in.

Demographics?

Yes, certainly.

Asset fundamentals? Definitely.

Most of the “risks” discussed in the newspapers today probably won’t matter 5 months from now, let alone 5 years! - If the consequences of making a mistake are unacceptable to you, seek independent, professional advice.

Only adopt evidence-based methodologies.

Only adopt evidence-based methodologies.ALSO READ: 2021, a year that defied the property odds

[ad_2]

Source link