[ad_1]

Predictions of the biggest property price fall in around 40 years have owners worried, first-home buyers salivating and mortgagees looking to refinance.

Doomsayers have been casting a pall over the optimists since before Nostradamus was boy but it’s hard to ignore the growing chorus of economics analysts looking into their crystal calculators and seeing harbingers of doom coming over the property horizon.

Over the past year Australian property has been the 13th fastest growing market in the world among the 56 measured by Knight Frank.

But its stellar performance in growing 18.3 per cent over the past 12 months was entirely down to the first three of the four quarters.

With a newly hawkish RBA now likely to hike interest rates from the floor to 2.5 per cent by the end of the year, banks, economists and property commentators are revising their housing forecasts markedly downwards, with material falls in home loans, credit growth, prices and building approvals foreseen.

ANZ economists predict interest rates may rise to as high as 2.35 per cent by the middle of next year.

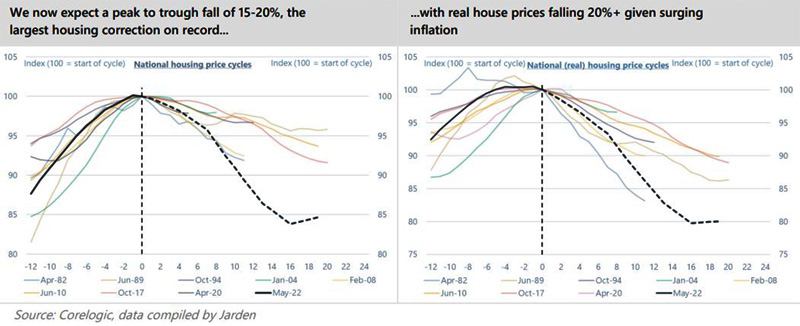

In response to the evolving landscape, investment and advisory group Jarden have released their predictions of what may happen within the housing and finance sector in the coming year and their conclusions are at least as negative as any other pundit’s.

Chief Economist Carlos Cacho said rising interest rates would lead to a reduction in borrowing capacity that would result in home loans falling by 25 per cent and a subsequent 15 to 20 per cent by the end of 2023.

The property price fall of up to 20 per cent nationally was better described as a collapse for Melbourne and Sydney, which Mr Cacho noted would be the worst affected.

“We now forecast prices will fall around 5 per cent by end-2022 and a further 10-15 per cent over 2023 (revised from minus 10 per cent) for a total 15-20 per cent peak-to-trough decline but falls in Sydney and Melbourne are likely to be larger and faster.

“This would be the largest house price correction since at least 1980, in both real and nominal terms, however, we expect regulatory easing to see a modest recovery in house prices from late-2023,” Mr Cacho said.

Rising rates, falling house prices, surging construction costs and the prior construction boom are also likely to see a material fall in building approvals.

“We now forecast a sharp fall in building approvals similar to the 2012 trough, before rebounding by the end of 2023, however, we believe completions/activity will not fall materially until mid-2023 given significant construction delays and the record pipeline of work yet to be done.”

Jarden’s crystal ball

The Commonwealth Bank has predicted prices falls of about 15 per cent over the next 18 months, and also singles out Sydney and Melbourne as the epicentres of the crunch.

ANZ senior economist Felicity Emmett said a quicker than expected lift in the cash rate could result in swifter and sharper property price falls, with a downside risk to the expectation of a 3 per cent drop in capital city prices this year and an 8 per cent decline next year.

AMP Capital chief economist Dr Shane Oliver expected average home prices would fall 10 to 15 per cent over 18 months, but said if he was to err, it would be towards even steeper drops.

Mortgage holders responding

Investors and owner-occupiers alike are already shying away from new loan commitments, with the value of new housing loans falling to 7.3 per cent for owner-occupier lending and 4.8 per cent for investor lending.

There are around 6 million properties with mortgages collectively worth around $2 trillion.

Aussies who bought their homes in the last five years have paid the highest prices ever, on the back of the booming housing market, particularly in 2021.

In findings released on Thursday (16 June), a leading finance information platform has conducted research to discover that half of Australian mortgagees may not have yet acted to help them better service their loans but are about to make changes.

Money.com.au found that the younger the mortgagor, the more likely they are to do something about it, with three-quarters of under-35s set to act.

When asked if they will make any changes when thinking about further interest rate rises and a slow economy, 51 per cent of respondents said yes.

Among these, 58 per cent said they will move at least part of their loan to a fixed interest loan. This includes 33 per cent that will move their whole loan to fixed rates. One in three (32 per cent) will refinance.

In contrast, just 9 per cent of respondents will make other major moves outside of their loans. Five (5) per cent said they will go so far as to sell their home, suggesting that Australia is unlikely to see a significant spike in homes hitting the market. Just 2 per cent will turn their home into an investment property and an equal 1 per cent will get help for their repayments from a family member or rent out a room in their home for additional income.

Licensed financial adviser and Money.com.au spokesperson Helen Baker said their research indicates Australians are willing to restructure their home loans to keep up with repayments and continue living in their property.

“More Australians want to be financially independent and responsible for their assets and are becoming more conscious and knowledgeable of how they need to navigate the current climate of increasing interest rates and inflation, against a downturn in the housing market in many parts of Australia.”

Ms Baker said borrowers that are currently in the best position are those that moved to fixed rates in the last few months.

“Even four months ago, you could get fixed rates that were lower than variable rates. I believe a large component of the 49 per cent of the respondents who will not act against rising rates have already refinanced or restructured their loans to put themselves in the best position financially.”

[ad_2]

Source link