[ad_1]

Mortgage rates are on the rise in Australia as funding costs and speculation about an RBA cash rate rise in 2022 puts pressure on banks.

While fixed rates lifted across the board, the big 4 banks have hiked more aggressively than many of the low-cost lenders.

While fixed rates lifted across the board, the big 4 banks have hiked more aggressively than many of the low-cost lenders.

In the past 4 months, CBA and Westpac have hiked interest rates 6 times, while NAB and ANZ have hiked 5 times.

Just on Friday, last week ANZ hiked its fixed rates for owner-occupiers paying principal and interest by 0.20 percentage points.

The bank also hiked investor and interest-only fixed rates by up to 0.66 percentage points.

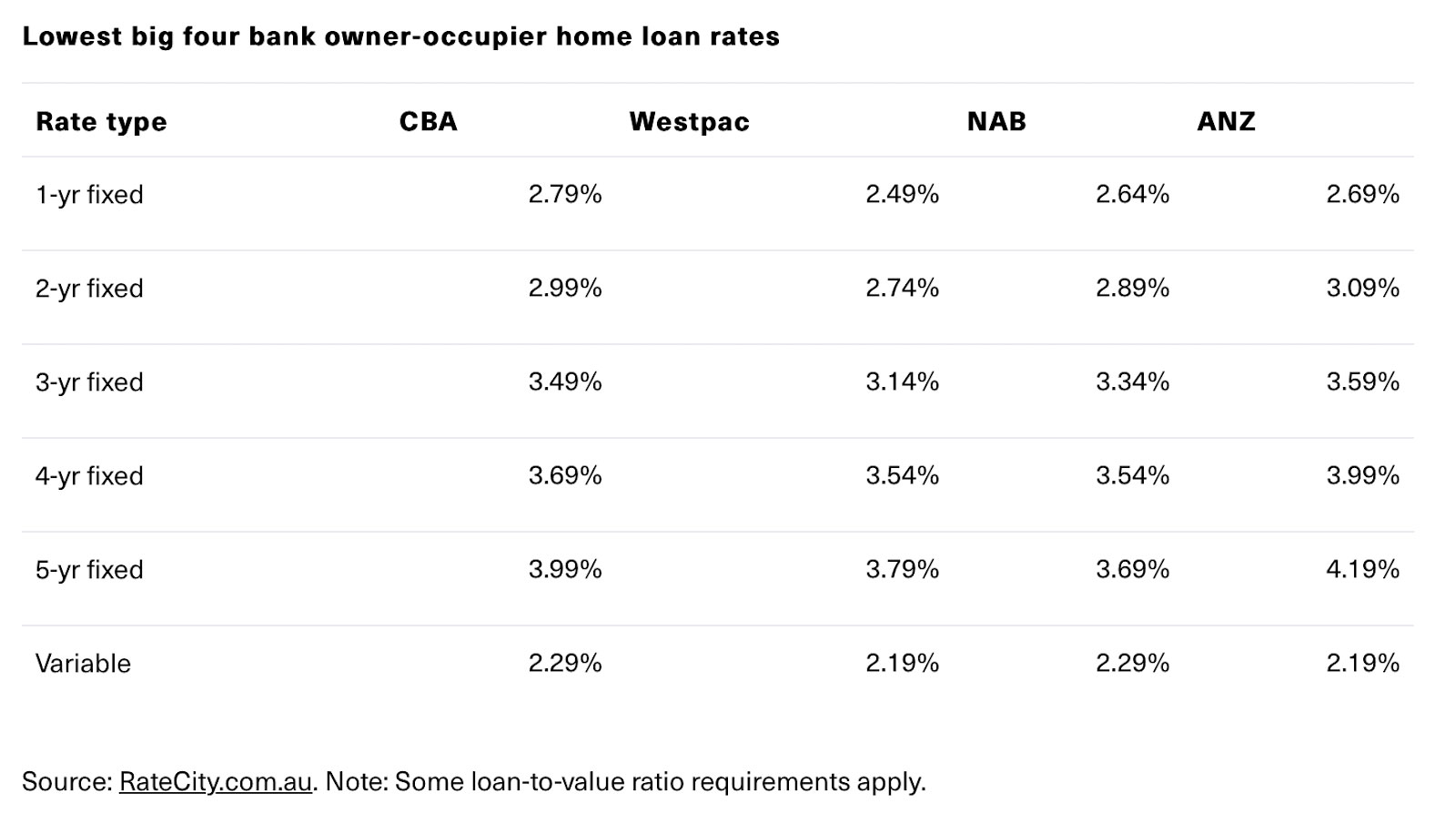

Here, comparison site Ratecity has put together a list of the lowest owner-occupier home loan rates available from the big 4 banks.

And the banks are warning that the increases aren’t over yet

They suggest that property owners could face higher mortgage repayments as early as June as financial markets and economists warn a rapid run-up in inflation could force the Reserve Bank to lift official rates above 2% within the next 12 months.

Combined with growing concern about the upcoming federal election and rising cost-of-living, CBA said it believed the Reserve Bank would have to start increasing interest rates by the middle of the year.

Even a 1% rise could add hundreds of dollars a month in repayments on the average new mortgage, the bank warned.

And such a hike is worrying news for homeowners and investors.

Now if you’ve been reading his regular blogs or watching his Property Insider videos you’ll know that neither Michael Yardney nor Dr. Andrew Wilson agree with this.

They believe low “real” wages growth will put a lid on “official” interest rate rises any time soon.

However, whether you’re planning to buy a new property or refinance an existing one, Ratecity’s latest list of the cheapest loans available should help.

Because it’s vital to know where to find the best value home loans, especially amid a rising market.

RBA rate hike — how much it could cost you

RateCity has crunched the numbers on CBA’s predicted RBA rate rises to determine how much existing variable rate mortgage holders may be impacted by rate rises.

RateCity has crunched the numbers on CBA’s predicted RBA rate rises to determine how much existing variable rate mortgage holders may be impacted by rate rises.

For a borrower with $500,000 owing on their mortgage with a rate of 2.96%, their monthly repayments could rise by $235 by the end of this year.

By February 2023, the same borrower could be paying $302 more a month than they currently are.

RBA rate hike — how it’ll affect borrowing capacity

Rising interest rates will significantly decrease how much banks will let people borrow.

Rising interest rates will significantly decrease how much banks will let people borrow.

This could also in turn dampen property prices as buyers who were planning to borrow at capacity will no longer be able to access as much money.

Based on CommBank’s predicted RBA rate rise forecast, RateCity research has discovered how much fewer people may be able to borrow.

If variable rates rise by 0.90% by the end of 2022 (cash rate hike to 1.00%), a single person earning $100,000 would be able to borrow an estimated $67,800 less (this assumes a 20% deposit).

ALSO READ: What’s wrong with Australian mortgages? They’re fixed for shareholders, not homeowners

[ad_2]

Source link