[ad_1]

The major banks are continuing to increase their home lending rates as new data reveals affordability is at its worst levels on record.

The major banks are continuing to increase their home lending rates as new data reveals affordability is at its worst levels on record.

With galloping property prices making it harder than ever for first homebuyers to get a foot on the property ladder, news of interest rate hikes is likely to only compound their fears.

Despite the Reserve Bank of Australia holding the official cash rate at historic lows, CommBank has just fuelled further fixed home loan rate rises, which sees those rates for owner occupied borrowers having risen by close to 1 per cent or more in just over four months.

The major bank’s two-year fixed rate for owner occupied borrowers has risen by 1 per cent since 14 October 2021, while its one, three, four and five-year fixed rates have risen by 0.80 per cent, 1.2 per cent, 1.3 per cent and 1 per cent respectively since 4 November.

This week’s changes include a whopping 0.25 per cent increase to CommBank’s three-year fixed rate for owner occupied borrowers, while its one and five-year fixed rates rose by 0.20 per cent and two and four-year fixed terms increased by 0.15 per cent.

RateCity.com.au research director, Sally Tindall, said the latest hikes from CBA show the bank is feeling the strain of sustained increases in funding costs.

“It’s hard to believe just five months ago CBA was offering a fixed rate loan below two per cent,” she said.

“Since then, CBA has hiked six times, raising most of its owner-occupier fixed rates above pre-pandemic levels.

“The big banks in particular have given up competing with the low-cost lenders on fixed rates.

“If customers want to fix with a big four bank today, chances are they’re going to have to pay more.

“There are still some relatively low rates from low-cost lenders, however, in this environment they’re unlikely to stick around for much longer,” Ms Tindall said.

The RateCity.com.au database shows there is just a single two-year fixed rate starting with a ‘1’, and just 14 one-year rates under this benchmark.

Despite inflation rising, the latest RBA minutes revealed they plan to keep the official cash rate at 0.1 per cent for much of 2022, at least.

Affordability crunch

With rates rising and prices still defying predictions of declines, many prospective home buyers have found themselves priced out of the game.

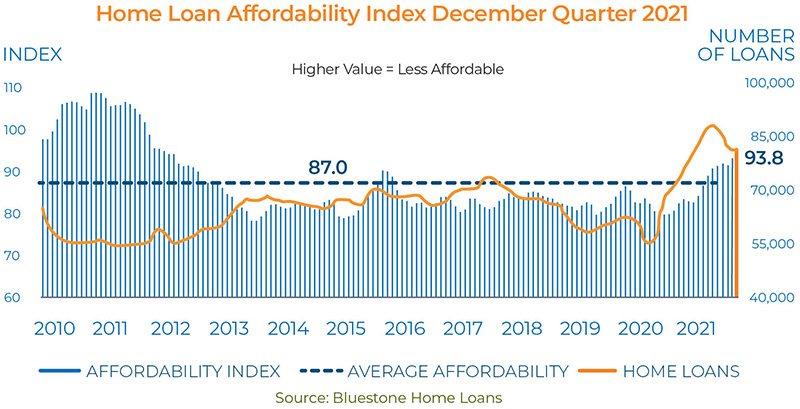

Bluestone Home Loans’ recently-released Home Loan Affordability Index for the December quarter confirmed that national home loan affordability fell dramatically in 2021 – a record calendar year decline of 14.5 per cent.

The December 2021 quarter Index result was 93.8 compared to 82.0 in the December 2020 quarter. The sharp fall in affordability is a result of booming house prices significantly increasing the average loan size required by buyers at the same time as wages growth remains stalled.

The latest result is also 1.2 points higher than the November quarter figure of 92.6 and above the long-term average of 87.0 (higher index numbers reveal a higher proportion of the average income required for the average home loan and reflect lower affordability.)

The Affordability Index has now tracked above the long-term average over seven rolling quarters to December 2021, and although the Index eased over October following six consecutive rises this reflected the transient impact of Covid restrictions.

Dr Andrew Wilson, consultant economist for Bluestone Home Loans, said strong home price growth over 2021 resulted in buyers borrowing more to keep pace with markets and, with subdued incomes growth and flat interest rates, this resulted in a higher proportion of buyer incomes required for loan repayments.

“Although home loan activity increased sharply again over December following November’s spike in activity, the late year revival reflects a catch-up from the restrictive impact on housing markets of severe spring coronavirus lockdowns – particularly in Sydney, Melbourne and Canberra.

“Last year’s runaway increase in prices is already moderating as stricter lending conditions from financial institutions place a ceiling on borrowing capacity, which has the effect of sidelining buyers, resulting in reduced demand and lower prices growth in the year ahead.

“But while the home loan boom may have ended, we believe the outlook for housing markets in 2022 remains generally positive, supported by recovering local economies, the ongoing easing of covid constraints and concerns, the resumption of high levels of migration, an underlying shortage of housing and continuing low interest rates.”

Dr Wilson said the high-priced Sydney and Melbourne housing markets continue to record significant declines in home price growth levels as a consequence of falling affordability reducing buyer activity and the satisfaction of pent-up demand.

“Brisbane and Adelaide, however, continue to report strong home buyer activity, which will act to offset overall home lending declines – although national volumes are set to be lower than the record levels of 2021.

“Owner-occupier and first home buyer loan activity will likely be lower over 2022 than the record levels reported over 2021, but we expect investor activity – which remains below the average of its long-term total residential loan market share – to continue to rise.”

[ad_2]

Source link