[ad_1]

New housing loan approvals fell 3.7% in February compared to the previous month.

Both owner-occupiers loans (-4.7% month on /month) and investors loans (-1.8% month on month) fell – but this is not surprising considering the slowing down in the housing market.

Despite the fall, the level of housing finance approvals are still 69% above pre-pandemic February 2020 levels.

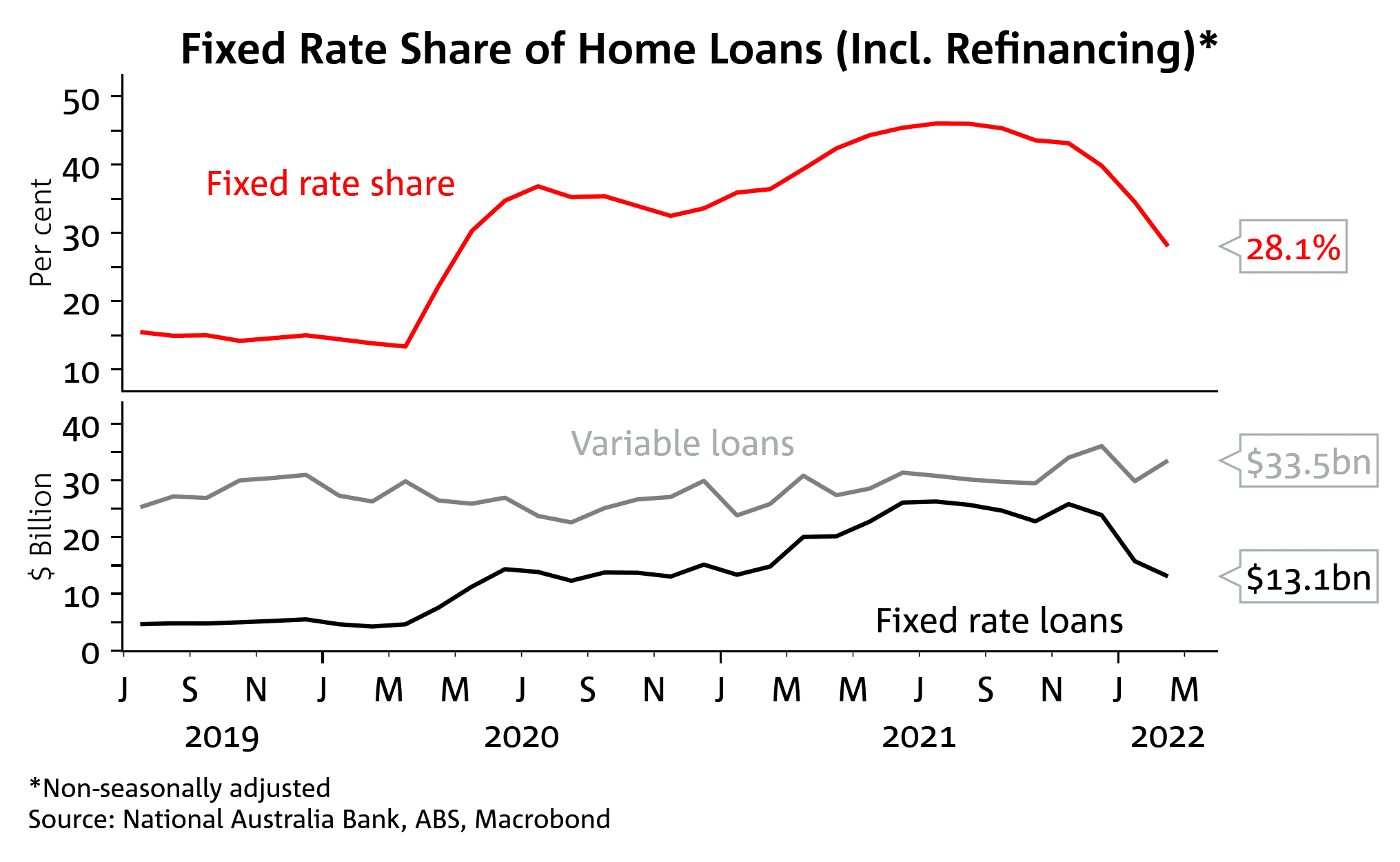

Lower share of fixed rate loans

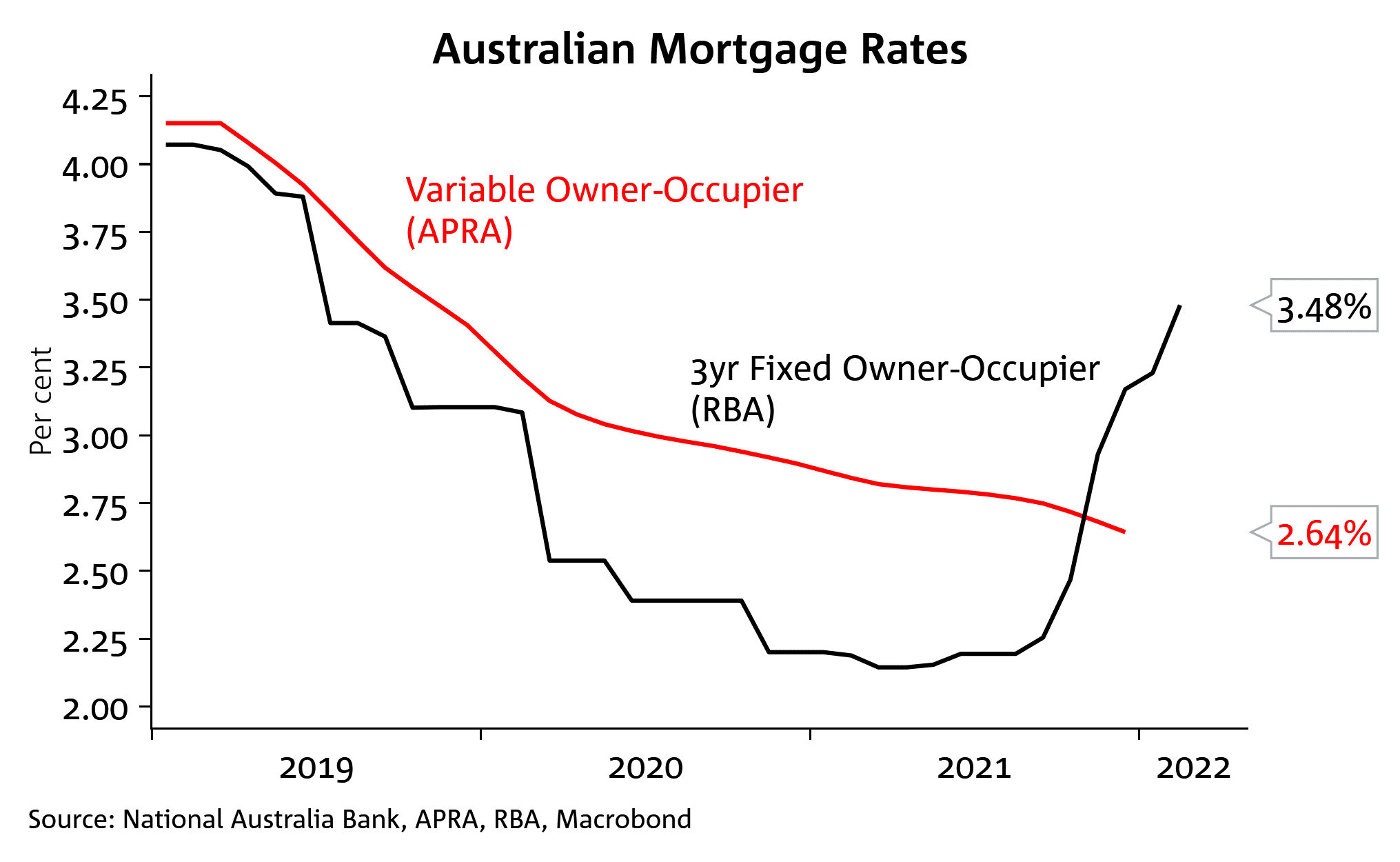

Higher fixed rates are starting to bite with the fixed rate share of new loan approvals falling to 28.1% from its recent peak of 46% in July 2021.

Prior to the pandemic the fixed rate share was around 15%, meaning a further pivot away from fixed rate loans is likely.

Some of the weakness in owner-occupier loans was driven by first home buyers (-9.7% month on month), but even excluding first home buyers, owner-occupier approvals fell (-3.1% m/m).

Some of the weakness in owner-occupier loans was driven by first home buyers (-9.7% month on month), but even excluding first home buyers, owner-occupier approvals fell (-3.1% m/m).

First home buyer loan approvals recorded a particularly big 8.3% fall with a steep 15.5% decline in NSW.

The decline in owner-occupier was broad-based

In contrast, construction-related loans were relatively steady in the month, reconfirming that the post HomeBuilder scheme has run its course and that the steep drop in dwelling approvals in January was an omicron-related rogue.

Of course, following the recent weather events in Queensland and NSW we are likely see some associated rebuilding in coming months.

This will likely show up in dwelling approvals but may not show in housing finance as much of this activity will be funded by insurance claims and government support.

The value of loans to investors recorded a milder 1.8% decline in February continuing the shift towards a higher share of investor loans in total activity.

Investor share is particularly high in South Australia, accounting for over half of new loans by value.

HomeBuilder unwind continues with the trend decline in new construction finance continuing

Investor share of approvals approaching long-run average levels

Source: Charts and commentary – NAB

[ad_2]

Source link