[ad_1]

National dwelling values rose 1.1% over January, up from the results seen in December (1.0%).

This uptick was almost entirely driven by the lower density sector with national house values increasing 1.3% in January, up from 1.2% in December, while unit value growth slowed from 0.4% to 0.3%.

This uptick was almost entirely driven by the lower density sector with national house values increasing 1.3% in January, up from 1.2% in December, while unit value growth slowed from 0.4% to 0.3%.

Despite this, both houses and units recorded a new cyclical high in annual appreciation, with values rising 24.8% and 14.3% over the 12 months to January respectively.

Figure 1 shows the rolling annual growth rate for national houses and units.

While annual house growth has generally outpaced unit growth over the past decade, the performance gap throughout the current upswing has been notably higher than in previous cycles, thanks in part to COVID-related demand shocks disproportionately affecting unit demand.

After peaking at 10.9% in September the annual performance gap narrowed over the final quarter of the year, in part due to the lifting of lockdowns and border restrictions as well as increasing affordability constraints diverting demand to the medium to high-density sector.

Despite this, this month’s house results saw the annual performance gap widen slightly, from 10.3% in December to 10.5% in January.

Despite this, this month’s house results saw the annual performance gap widen slightly, from 10.3% in December to 10.5% in January.

One possible explanation for this is the disparity between the advertised house and unit supply.

A feature of the housing market throughout the COVID period to date, shortages in advertised listings have helped fuel value growth by creating a sense of urgency amongst buyers.

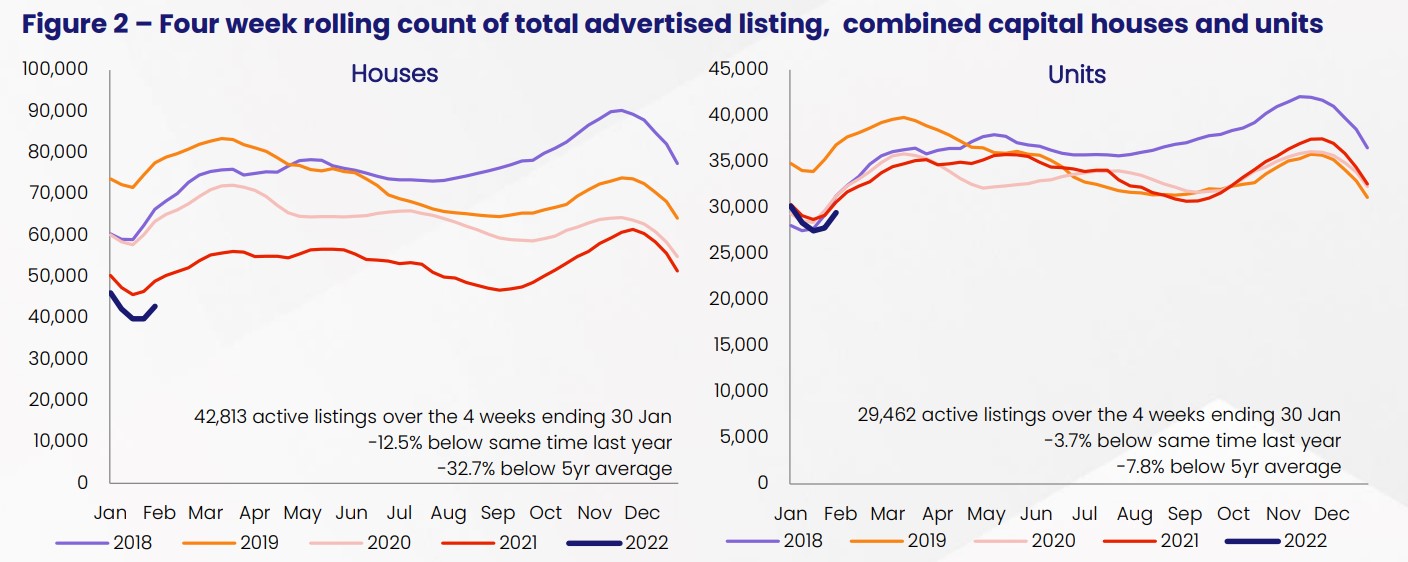

Figure 2 shows the 4-week rolling count of total listings for the combined capital cities houses and units.

Over the 4 weeks to 30 January, the combined capital cities total advertised unit supply was down -3.7% compared to the same time last year and -7.8% below the previous 5-year average.

Over the same period, capital city house listings were down -12.5% compared to this time last year and – 32.7% below the 5yr average.

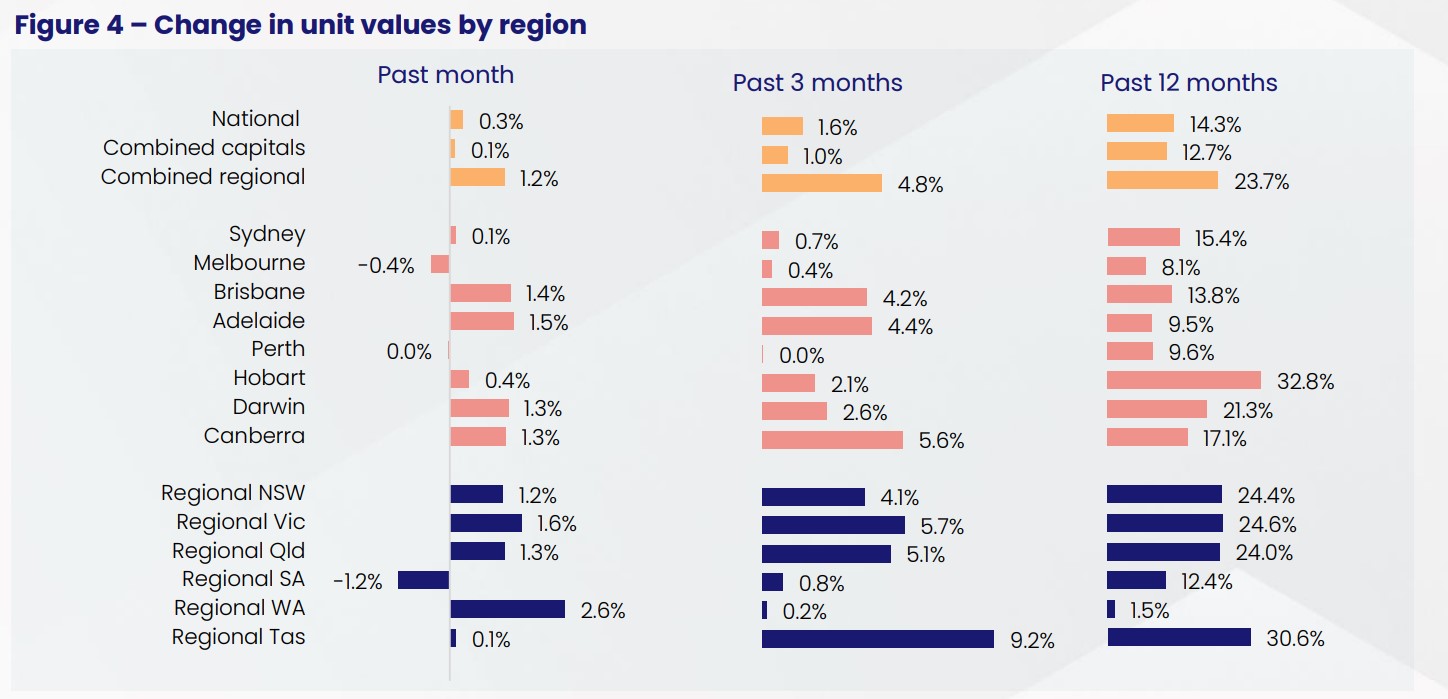

While unit growth has continued to underperform nationally, growth conditions are becoming more diverse amongst the individual capitals and rest of state regions.

Canberra (5.6%) Darwin (2.6%), regional Victoria (5.7%), and regional Tasmania (9.2%) all recorded stronger unit growth over the three months to January than their lower density counterparts (3.2%, -0.2%, 5.2%, and 6.0% respectively) while Hobart units recorded an annual appreciation of 32.8% compared to a 26.3% capital gain for houses.

With the exception of Darwin, each of these markets’ total advertised unit stock was more than -30% below the 5-yr average.

A multi-speed dynamic is beginning to emerge across the combined capitals.

Adelaide led the pace for unit gains, recording a monthly rise of 1.5% followed by Brisbane (1.4%).

Unlike the other capital markets, the pace of growth in Brisbane and Adelaide is yet to show signs of a slowdown in momentum, with each city recording a new cyclical high over the 12 months to January (13.8% and 9.5% respectively).

Melbourne recorded a modest fall in unit values, down -0.4% through January, while Perth values remained flat over the same period.

Sydney values rose 0.1% over January following the -0.2% decrease in values recorded in December.

Conditions were even more diverse amongst the regional markets with units in regional WA recording a monthly rise of 2.6%, while values fell -1.2% in Regional SA over the same period.

Regional unit markets offering a lifestyle or sea change such as Tasmania’s Launceston and North East region (33.9%) recorded the strongest annual growth, followed by the Sunshine Coast in Queensland (31.1%), and the Mid north coast (28.5%), and Richmond – Tweed (28.5%) in NSW.

Over the same period, units in Bunbury in WA recorded an annual depreciation of -8.3%.

Regional growth dynamics are explored further in the February edition of CoreLogic’s Regional market update.

Bucking the trend seen since May 2019, national unit rents recorded a higher monthly growth rate compared to houses in January, up 1.0% and 0.7% respectively.

Similar monthly growth was recorded across the combined capital cities, while both regional houses and units recorded a monthly rental rise of 0.8%.

Despite the lower monthly growth rate, regional growth continues to outpace capital city rents at the annual level, rising 12.1% over the 12 months to December, compared to the 6.7% rise recorded across the capitals.

Despite the lower monthly growth rate, regional growth continues to outpace capital city rents at the annual level, rising 12.1% over the 12 months to December, compared to the 6.7% rise recorded across the capitals.

January’s strong unit rental performance was led by Melbourne (1.4%) and Sydney (1.1%).

Which had previously seen rental values decrease 8.2% and 7.2% between March and December of 2020.

Compared to the other capitals, these two cities’ unit rental markets were disproportionally affected by stalled overseas migration and the shift in domestic rental preferences towards lower density options through the pandemic.

Despite strong growth in recent months, Melbourne unit rents were still -4.2% below their pre-COVID level, while Sydney’s rents are up just 1.0%.

At the other end of the spectrum, markets like Darwin, Hobart, and Regional Tasmania, which had recorded strong rental growth throughout the COVID period, are now recording negative monthly results (-0.9%, -0.2%, and -0.2% respectively).

With the gap between capital gains and rental growth remaining lower amongst units compared to houses, national unit yields (3.68%) remain 62 basis points above house yields (3.06%), with units outperforming houses across each of the broad regions of Australia.

Unit yields have remained relatively stable since October, but are down 30 basis points compared to this time last year, while house yields are down 53 basis points annually.

Unit yields have remained relatively stable since October, but are down 30 basis points compared to this time last year, while house yields are down 53 basis points annually.

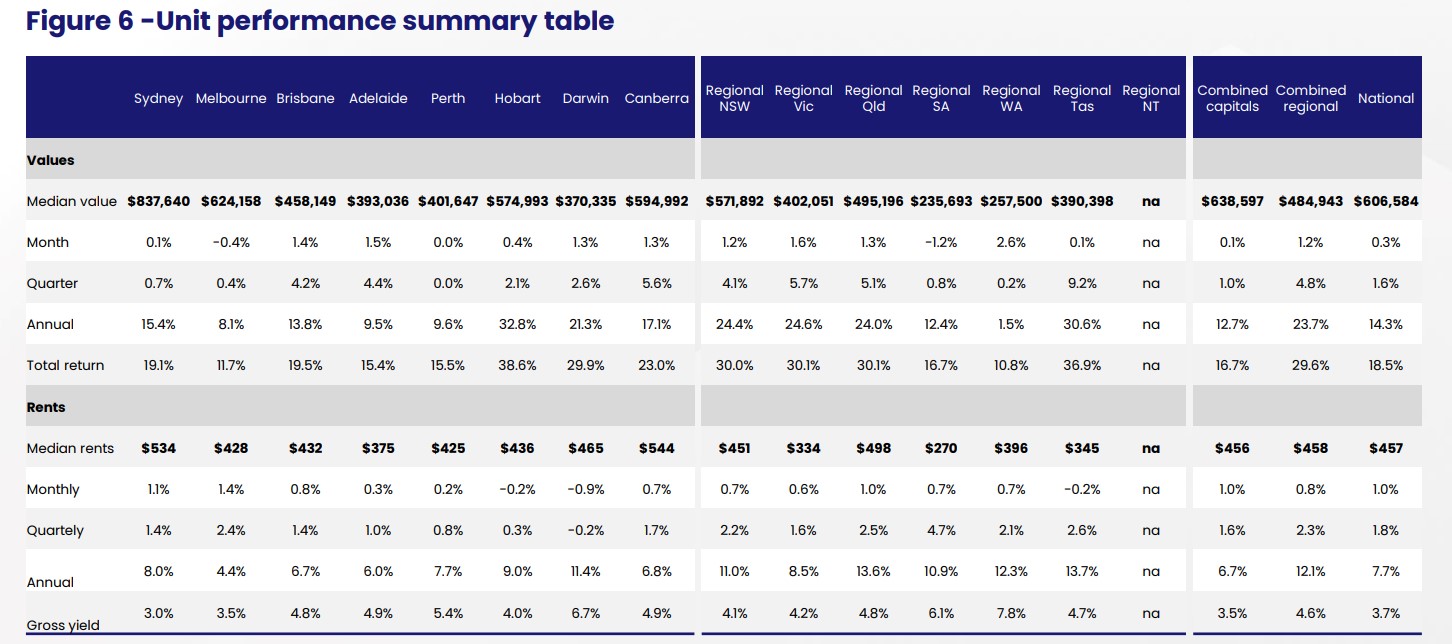

Figure 6 compares the January gross rental yields across unit markets to those recorded this time last year.

All unit markets recorded a decrease in their rental yield, except for regional WA and regional SA which saw yields rise from 7.61% and 5.95% in 2021 to 7.80% and 6.13% in 2022.

The most expensive unit markets of Sydney (3.01%) and Melbourne (3.52%) recorded the lowest gross rental returns, while the relatively cheaper markets of Regional WA (7.80%), regional NT (7.11%), and Darwin (6.70%) recorded the highest yields.

Following on from the slowing of growth seen in the back half of 2021, the 2022 housing market appears to be starting the year in a similar position, with market conditions becoming increasingly diverse, while capital gains remain positive, albeit slowing.

With a headline inflation rate of 1.3% over the December quarter, the prospect of a rate hike in mid-to-late 2022 presents a clear downside risk for housing values.

Similarly, affordability constraints, coupled with tighter lending restrictions, are seeing more and more prospective buyers being priced out of the market.

Similarly, affordability constraints, coupled with tighter lending restrictions, are seeing more and more prospective buyers being priced out of the market.

Despite this, some tailwinds for the Australian unit market do exist.

Three of the eight capital cities are now boasting a median house price above the $1 million mark (Sydney, Melbourne, and Canberra), and the difference between a national house and unit values recorded a new all-time high in January (28.3%).

It is likely affordability constraints will gradually deflect more demand away from the more expensive house segment, towards the more affordable medium to low-density sector.

With international borders opening fully on the 21st of February, Australia may gradually see a return to pre-COVID levels of migration.

As most migrants initially rent in Sydney or Melbourne this could help bolster rental demand in those markets hardest hit by the pandemic, which, in turn, could boost investor demand.

[ad_2]

Source link