[ad_1]

A year ago, first home buyer activity was at a peak and riding a wave propelled by low mortgage rates and government incentives but one year on this market is being crunched.

A year ago, first home buyer activity was at a peak and riding a wave propelled by low mortgage rates and government incentives.

Fast forward 12 months and more stringent lending requirements, brutal house prices and investor pressure have diminished first home buyer activity.

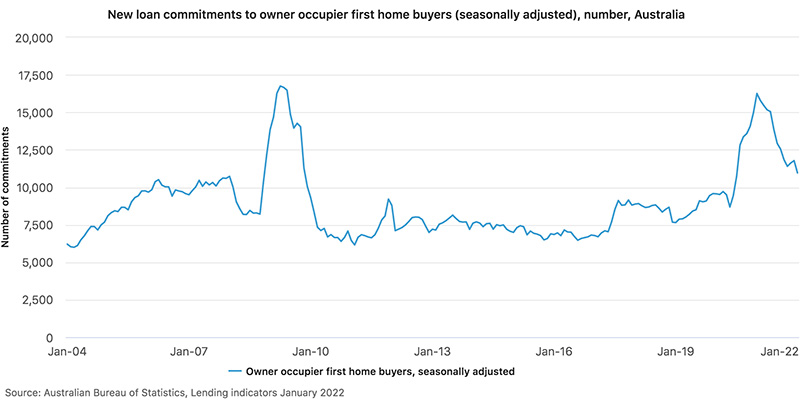

January 2022 saw a drop in participation to just under 11,000 compared to more than 16,000 for the corresponding time last year, according to Australian Bureau of Statistics data.

First-home buyers can be excused for thinking that skipping avocado on toast won’t suffice when it comes to financing their dream of home ownership, let alone their dream home.

CoreLogic data shows the average Aussie home value increased in the last month alone, by $173,805, up to $728,034, having increased at their highest rate in two decades in 2021.

All states and territories recorded drops in first homebuyer loan commitments at the start of the year, with the biggest declines seen in Queensland by 16.1 per cent while the ACT bucked the nationwide trend and rose 25.7 per cent.

Even by global standards, first-home buyers in Australia are being crunched.

Sydney, Melbourne, Adelaide, Brisbane and Perth were recently ranked as the 2nd, 5th, 14th, 17th and 20th least affordable cities in the world respectively, according to Demographia’s International Housing Affordability 2022 Edition.

Sydney median house prices are rated in that report as currently 15 times more than the average household income. Given most first-home buyers are struggling to earn the average wage, their situation is even harsher.

According to Domain’s First Home Buyer Report for the December quarter, a Sydney couple aged 25 to 34 on the average income for that age group, saving 20 per cent of monthly post-tax income, would require more than eight years of income to buy an entry-level property. This is an extra 18 months compared to just a year ago.

The time required to save for an entry-level Melbourne house has in one year blown out by six months to six and a half years, according to the report released Wednesday (23 March).

Belle Property Killcare, NSW principal Cathy Baker

Cathy Baker, principal of Belle Property Killcare, NSW, located over an hour north of Sydney, says one of the challenges for first-home buyers is they are priced out of city areas and now also out of most large regional towns.

“This is forcing many home buyers into rentals or into buying interstate or into remote regional areas,” Ms Baker said.

“First-home buyers also compete with investors looking for opportunities for improvement and are often outbid in this situation.

“Market increases in most regional areas have meant first-home buyers have had to focus their searches further out to get value or look at using a guarantor with parents.”

The Federal House of Representatives Standing Committee on Tax and Revenue’s report released March 18, (The Australian Dream: inquiry into housing affordability and supply in Australia) acknowledges one of the largest barriers for first-home buyers is saving for a deposit.

Sydney-based Zippy Financial’s Director and Principal Broker, Louisa Sanghera, points to minor adjustments to mortgage serviceability calculations as not having significantly changing loan approvals but highlights prospective property owners must show genuine savings.

“Lenders always want to see a genuine savings history, including funds that represent at least five per cent of the property’s purchase price,” Ms Sanghera said.

“Banks generally recognise that it is difficult to save the deposit for your first

property, because of the added expenses of paying rent.

Zippy Financial director and principal broker Louisa Sanghera

“However, it is never a bad thing for any potential borrower to show that they have been diligently saving funds over a period of time, even if those funds represent only five per cent of the purchase price.”

The Standing Committee also recommended that first-home buyers be allowed to use their superannuation assets as security for a home loan.

“This type of scheme will avail the option of home ownership to more people, which must be a good thing – depending on the finer details of the policy,” Ms Sanghera said.

“We already have stamp duty concessions and various schemes in place, yet fewer people can get into the market.”

Housing models such as rent-to-own and build-to-rent, replacing state and territory governments stamp duty with land tax and a government review on how transitional costs regarding stamp duty might be smoothed, were other recommendations made by the Federal report.

“Ultimately, the reforms need to target the needs of first-home buyers, Real Estate Institute of NSW (REINSW) CEO Tim McKibbin said.

“Enabling first-home buyers to access more money merely increases the debt they will have to service,” he said.

“Instead, alleviating the tax burden on this cohort will make property more affordable, help them service a loan more appropriate for them, while not inflating prices.

“This latest inquiry into housing affordability is not the first and findings of past inquiries remain unaddressed or have focused on demand strategies, which will not solve a supply problem.”

LJ Hooker Launceston Tasmania principal and licensee Justin Goebel

Principal and Licensee of LJ Hooker Launceston Tasmania, Justin Goebel, said times are extremely difficult for first-home owners throughout Tasmania.

“Price rises and low stock levels mixed with high buyer activity give sellers the luxury of increased offers, making it very difficult for first-home owners.”

“Investors from all around the country have shown high interest in Tasmanian properties, enquiries for people looking to move from the larger cities to the likes of Hobart and Launceston have dramatically increased, not to mention your mum and dad buyers who own their home or are looking to upgrade into a larger home, contributing to the property fiasco throughout the state,” he said.

“Home ownership is becoming very difficult to obtain due to the increase of house prices, to the point that renting or staying at home with mum and dad has become the only alternative, while hoping for the market to become more affordable.”

Despite the volatility for first-home buyers, Ms Sanghera feels first-home buyer activity has remained elevated compared to the past decade.

“Stimulus measures such as the HomeBuilder Scheme did bring forward the buying decisions of many first-time buyers, but they remain highly active in the market, even after last year’s strong property price growth.”

Cathy Baker has seen many first-home buyers who bought in 12 months ago experience amazing growth, allowing them to fall back on the equity in their properties to do further improvements or borrow for improvements or resale.

She says strategies for success in the current climate include looking for properties to which a first-home buyer can add value.

“That’s properties in original condition, that are structurally sound – consider a duplex with no strata or investigate high growth regional areas where the prices provide great return and look at renting closer to home.

“Within two years they can capitalise on the equity and improvements and borrow to do further improvements or resell,” she said.

Justin Goebel believes it is becoming more common for parents to dip into equity to get the deal done for their children.

“Purchasing the ‘great Australian dream’ is unfortunately becoming just a dream for many,” he said.

Research by Finder backs up this trend, showing 28 per cent of Millennials and 25 per cent of Gen X have not moved out of their childhood home by age 30, compared to 8 per cent of Baby Boomers.

“Many young people are concerned that unanticipated price growth over the last couple of years has ruined their chances of buying a home,” Finder Senior Editor Sarah Megginson said.

[ad_2]

Source link