[ad_1]

End of a low-rate era The lowest fixed home loan rate on record has been increased this week, unfortunately ending the ultra low rates we’ve been accustomed to.Greater bank lifted their 1-yr rate of

The lowest fixed home loan rate on record has been increased this week, unfortunately ending the ultra low rates we’ve been accustomed to.

Greater bank lifted their 1-yr rate of 1.59% to 1.89% for owner-occupiers paying principal and interest making 1.79% the new lowest rate on the market available from UBank, Qudos Bank and RACQ for 1 year.

Sally Tindale, research director at RateCity.com.au said it was unlikely we would see interest rates as low as 1.59% again, and that the hike from Greater Bank marked an end of an era for record-low fixed rates.

Lowest owner-occupiers rates on RateCity.com.au

| Lender | Advertised rate | |

|---|---|---|

| 1yr fixed | Qudos Bank, RACQ, UBank | 1.79% |

| 2yr fixed | HSBC | 1.88% |

| 3yr fixed | Australian Mutual Bank | 1.98% |

| 4yr fixed | BankVic | 2.39% |

| 5yr fixed | BankVic | 2.49% |

| Variable | Reduce Home Loans | 1.77% |

Source: RateCity.com.au. Note Rates are for owner-occupiers paying principal and interest, LVR requirements apply for some loans.

Lowest big four bank owner-occupier home loan rates

| CBA | Westpac | NAB | ANZ | |

|---|---|---|---|---|

| 1yr fixed | 2.54% | 2.34% | 2.54% | 2.39% |

| 2yr fixed | 2.69% | 2.49% | 2.69% | 2.59% |

| 3yr fixed | 3.14% | 2.89% | 3.14% | 2.99% |

| 4yr fixed | 3.34% | 3.19% | 3.34% | 3.39% |

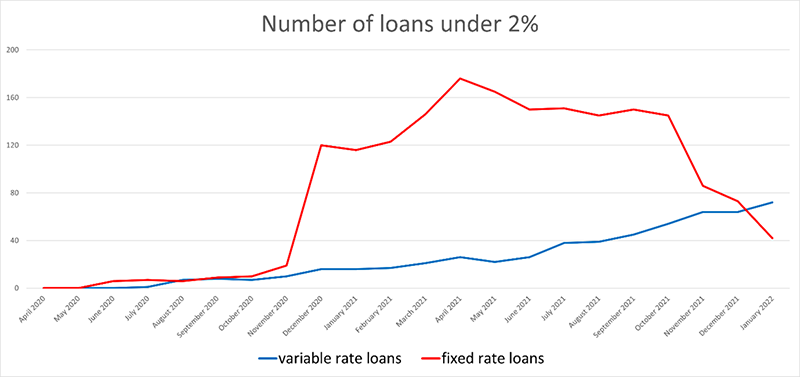

More than half of all lenders have hiked at least one fixed rate in the past two months, with only 41 fixed rates under 2%, this is expected to fall to zero (or close to) within the next six months according to RateCity.com.au.

“At the beginning of 2021, there were 117 fixed rates under 2 per cent. This number peaked in April at around 180 but has plummeted in the last couple of months. While there are still 41 fixed rates under 2 per cent, the list is shrinking quickly. We expect the majority of these to be gone within the next six months,” Ms Tindale said.

“While we expect more cuts to variable rates in the next few months, we could see some lenders hike later this year ahead of the RBA, if the cost of funding continues to escalate.”

Lenders that have moved at least one rate in the last 2 months

| Rate type | Lenders that have cut | Lenders that have hiked |

|---|---|---|

| 1yr fixed | 20 | 52 |

| 2yr fixed | 7 | 65 |

| 3yr fixed | 1 | 75 |

| 4yr fixed | 1 | 44 |

| 5yr fixed | 2 | 63 |

| Variable | 47 | 4 |

Source: RateCity.com.au. Note some lenders have moved more than one rate. Date range is from 12 November 2021 to 11 January 2022.

Home loan rates under 2%

| Rate type | Number of rates under 2% |

|---|---|

| 1yr fixed | 26 |

| 2yr fixed | 14 |

| 3yr fixed | 1 |

| 4yr fixed | 0 |

| 5yr fixed | 0 |

| Variable | 72 |

Source: RateCity.com.au.

Source: RateCity.com.au.

Home loan customers looking to secure a fixed interest rate are also being ‘trapped’ by banks that are lifting their rates before the new loans have been approved and settled according to Cara Giovinazzo, owner of Queensland finance brokerage Borro.

Ms Giovinazzo said she was receiving complaints from customers of banks increasing their rates after they had signed up for a fixed rate offering.

“Some customers are being caught out by the big banks lifting their fixed rates and I have one client who has lodged a formal complaint after his rate was increased three times before the loan was approved,”

“He made the decision to go with that bank based on their rate, and with his settlement date approaching, he does not now have the luxury of time to change lenders, effectively trapping him.” Ms Giovinazzo said.

Banks have been taking weeks, if not months to settle loans and this sort of practice can potentially cost customers thousands if rates are lifted during the process.

“We have seen a frenzy of fixed rate increases by the big banks with the Commonwealth Bank raising rates four times in just two months, with more than a whole percentage point added to its four-year fixed rate since the middle of October.”

Ms Giovinazzo said although the Reserve Bank of Australia (RBA) has stated it doesn’t see conditions for a rise in the current official interest rate of 0.1 per cent until 2024, some economists expect the RBA to act sooner while there are also predictions of banks lifting rates out of cycle due to cost of funding issues.

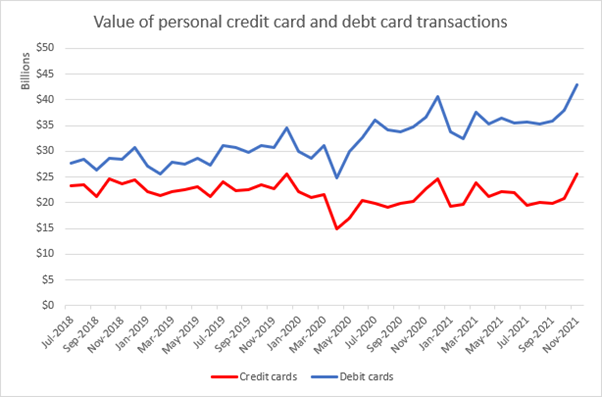

RBA data also shows Australians have been over $25 billion worth of transactions on their credit card in November, the highest value since 2002. Debit card transactions were also hitting record highs at the end of 2021 hitting over $43 billion, totaling almost $69 billion on both personal credit and debit cards.

The east coast of Australia had come out of lockdowns, COVID cases were relatively low and big retailers were offering discounts in the Click Frenzy, Black Friday and Cyber Monday sales which could have attributed to the record highs, however this debt accruing interest in credit cards has risen $74.8 million month-on-month – the first time it’s gone up since May 2021.

“Australians went on a post lockdown spending-spree, making the most of being able to go to the shops in the pre-Christmas sales.”

“The issue for many Australians who overspent on their credit cards or buy now pay later accounts is that they may now have trouble paying it all back.” Said Ms Tindall.

“This problem could get worse over the next couple of months, especially for people impacted by COVID who haven’t worked the hours they were expecting to.

“Anyone struggling to make their credit card or buy now, pay later repayments should call their provider and ask for help before getting stung with late fees and interest charges,” she said.

Credit card statistics: personal credit cards in November 2021

| Amount | Monthly change | Year-on-year change | |

|---|---|---|---|

| Number of accounts | 12.4 million Lowest since Dec 2006 |

-731 -0.01% |

-449,616 -3.5% |

| Value of purchases | $25.27 billion Highest on record |

+$4.78 billion +23.3% |

+$2.90 billion +12.9% |

| Value of transactions | $25.70 billion Highest on record |

+$4.86 billion +23.3% |

$2.92 billion +12.8% |

| Balances accruing interest | $17.16 billion | +$74.8 million +0.4% |

-$2.48 billion -12.6% |

Source: RBA, released 12 January 2022, original data, excludes commercial cards. Monthly change is October to November 2021, year-on-year change is Nov 2020 to Nov 2021.

Debit card statistics: November 2021

| Amount | Monthly change | Year-on-year change | |

|---|---|---|---|

| Number of accounts | 36.3 million | +144,746 0.4% |

+1.4 million +4.0% |

| Value of purchases | $42.21 billion Highest on record |

+$4.87 billion +13.1% |

+$6.32 billion +17.6% |

| Total value of transactions | $43.01 billion Highest on record |

+$4.98 billion +13.1% |

+$6.34 billion +17.3% |

Source: RBA, released 12 January 2022, original data. Monthly change is October 2021 to November 2021, year-on-year change is November 2020 to November 2021.

Source: RBA

Comparison Rate Warning: The comparison rate is a way of comparing loans by including both the advertised rate and the fees involved. The comparison rates are based on credit of $150,000 and a term of 25 years for home loans, and based on credit of $30,000 for a term of 5 years for personal and car loans, unless otherwise indicated, and represents the effective rate on the loan. Comparison rates are not calculated for revolving credit products. Comparison rates are not required for revolving credit products such as overdrafts and line of credits, as these products are not paid down gradually like a normal loan, which means the fees have a different impact on the overall cost of the loan. WARNING: This comparison rate is true only for the example given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. The source of this data was provided by RateCity.com.au at the data of publish and maybe subject to change.

Disclaimer: All information provided is of a general nature only and does not take into account your personal financial circumstances or objectives. Before making a decision on the basis of this material, you need to consider, with or without the assistance of a financial adviser, whether the material is appropriate in light of your individual needs and circumstances. This information does not constitute a recommendation to invest in or take out any of the products or services.

[ad_2]

Source link