[ad_1]

Please use the menu below to navigate to any article section:

Capital cities, regional areas, houses, and units all saw an increase in rents last quarter, culminating in the highest calendar year growth rate since 2007.

CoreLogic’s quarterly Rental Review shows the national rental index increased 1.9% during the December quarter, a repeat of the figures recorded in the September quarter.

Despite quarterly growth rates easing since peaking in March at 3.2%, the national index recorded its highest annual growth rate since January 2007 in November at 9.44%, before falling slightly in the 12 months to December at 9.40%.

Rents were under extraordinary pressure from many factors, not least the demand for detached housing and an ongoing lack of rental supply.

For more than 18 months we’ve seen demand for detached housing continue unabated as more renters work from home, either on a permanent or now hybrid working arrangement, which drives demand for more spacious living conditions.

In addition to this trend, investors, while still active in the market, have been dwarfed by an over-representation of owner-occupiers entering the market, upgrading or buying holiday homes that aren’t being added to the rental pool.

This is also being played out in the rapid growth in regional rental markets.

Regional rents

Regional rents continued to outpace capital city rents over the fourth quarter with regional dwellings rising 2.5% against the 1.6% rise in capital city rents, taking the annual regional rental growth rate to 12.1%.

Over a 10-year period, regional house rents have increased 33.2% compared to 24.9% growth across the combined capitals.

The regional unit market has seen rents increase 41.4% in the past decade compared to capital city figures of 14.4%.

The stronger rental conditions across the regional markets is a story involving both demands as well as supply, following a surge in regional population growth through the pandemic, especially across regional Victoria and regional NSW.

While demand has risen we generally haven’t seen much of a supply response.

Australia’s rental market is mostly reliant on private sector investors to provide rental housing.

Investors as a proportion of total mortgage demand moved through record lows in early 2021, highlighting relatively low levels of investment activity across the country and also implying relatively low levels of new rental stock coming onto the market.

Arguably the regions have less elasticity in rental markets, meaning, when demand rises, supply is less responsive than capital cities where investors are generally more active.

Brisbane was the strongest performing rental market amongst the capitals over the quarter, rising 2.3%, followed by Canberra and Hobart, both rising 2.1%.

Despite recording the strongest annual rental growth (15.2%), the Darwin rental market was the worst performing over the quarter, with rents rising 0.6% over the three months to December.

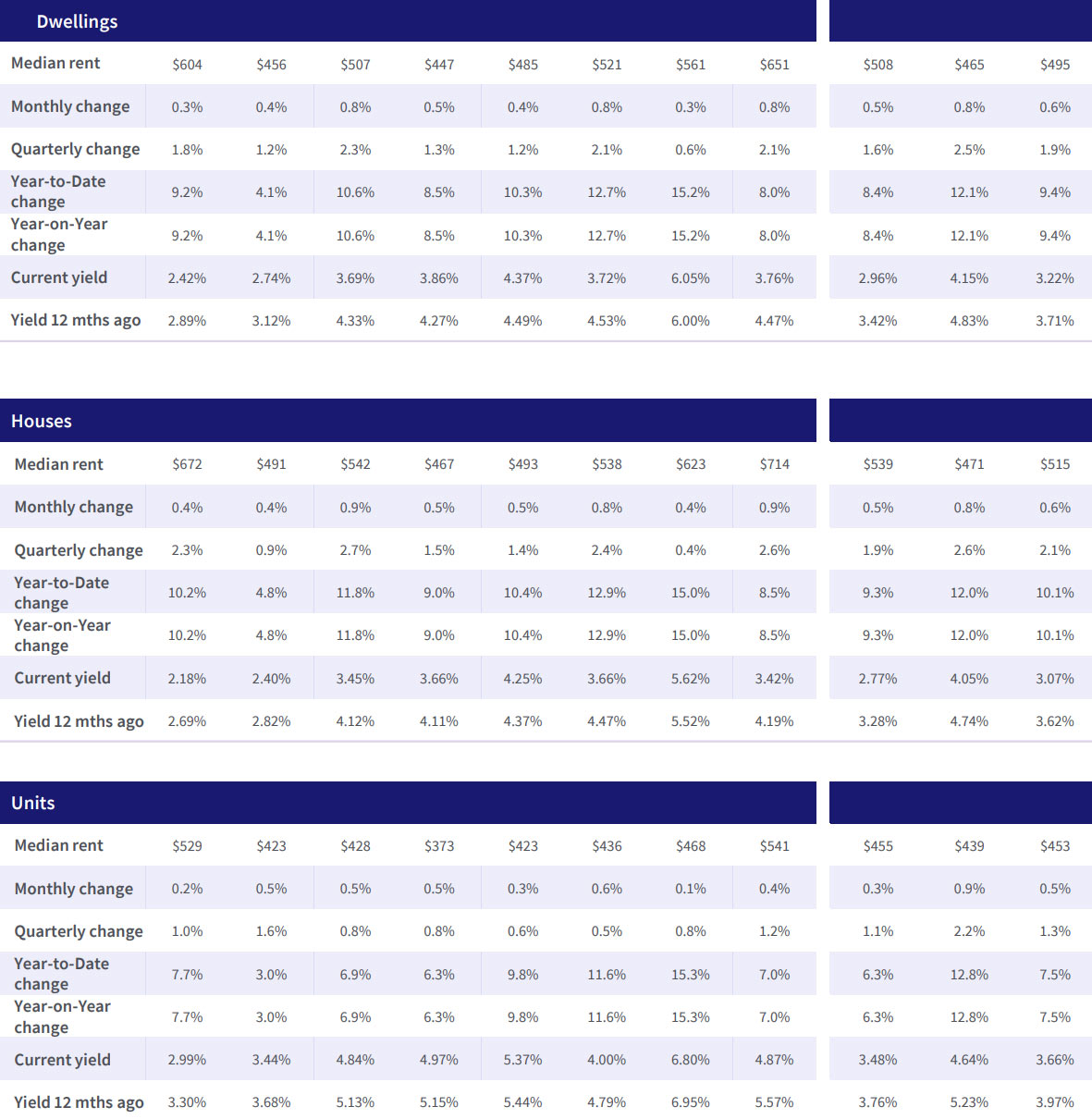

Canberra remains the most expensive capital city rental market, with typical dwellings renting for $651 per week, followed by Sydney ($604p/w), Darwin ($561p/w), Hobart ($521p/w), and Brisbane ($507p/w).

Adelaide remains Australia’s most affordable capital with a median dwelling rent of $447 per week, followed by Melbourne at $456 per week.

Houses vs Units

Each capital city market posted a rise in rents over the December quarter for both houses and units.

Brisbane recorded the strongest quarterly increase in house rents of 2.7%, taking annual growth rates to 10.6%.

Darwin house rents increased 0.6% during the quarter, however, its growth in rents during the first half of 2021 resulted in the highest annual house growth figures of any capital at 15.0%.

As arguably the most COVID-impacted unit market in Australia, Melbourne’s rental growth trends shifted in December, as units recorded the strongest rental growth in the country, up 1.6%.

Melbourne’s rents remain 5.5% below the record highs of July 2019, however, any recent momentum in unit rental growth could represent a recovery trend, underpinned by affordability constraints.

Brisbane’s rental market for houses has shown strength throughout the pandemic as demand outweighed supply, while Melbourne’s unit market has been weak through most of the pandemic to date due to low demand against relatively high vacancy rates.

Melbourne’s unit market is now benefiting from higher demand as more domestic renters seek out affordable housing options in the unit sector.

Demand for Melbourne unit rentals is likely to increase more sharply as foreign students and international visitors return.

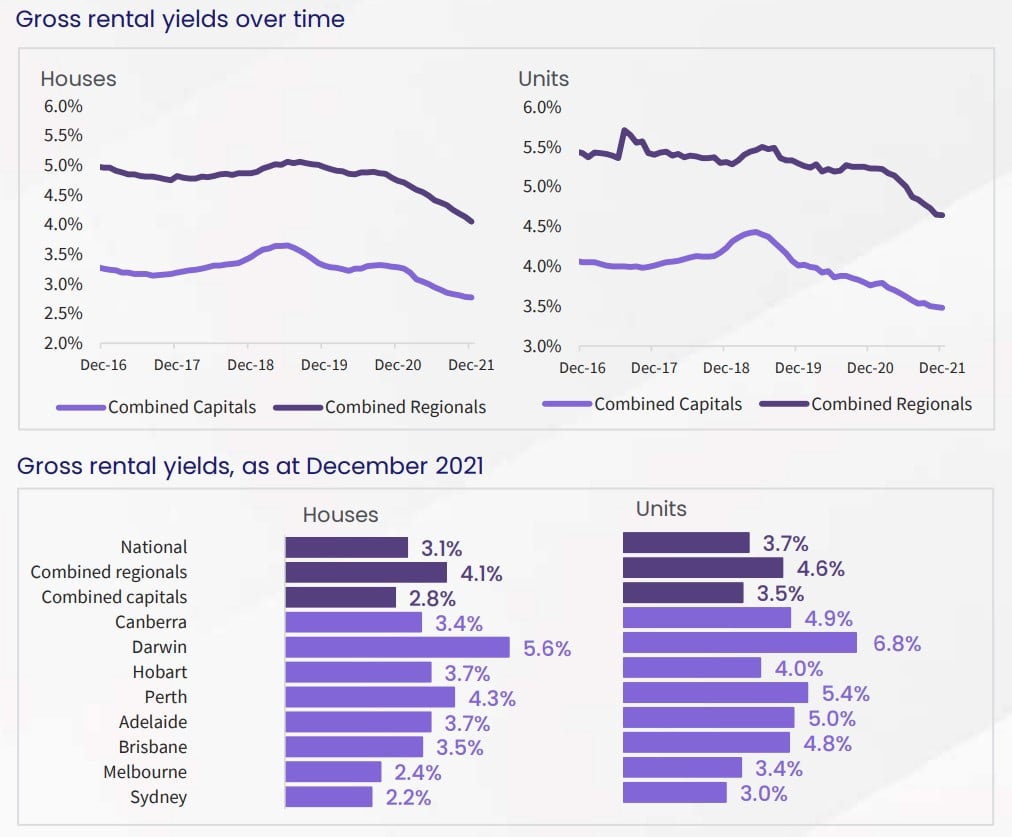

Rental yields

Gross rental yields continued to slide in December, hitting a new record low as the growth in dwelling values outpaced rental increases.

While national dwelling values rose 3.9% in Q4 of 2021, rental values increased 1.9% causing gross rental yields to fall to 3.22%.

COVID restrictions such as international border closures, and disruption to employment across sectors such as tourism and hospitality, which have a relatively high proportion of renters, have played a role in compressed yields.

Sydney and Melbourne have the lowest yields of any capital city at 2.42% and 2.74% respectively while Darwin has the highest at 6.05%, followed by Perth (4.37%).

Most expensive and most affordable suburbs

CoreLogic’s quarterly Rental Review includes a list of the country’s top 30 most expensive and affordable rental suburbs for each capital city as well as all key rent and yield statistics.

CoreLogic’s quarterly Rental Review includes a list of the country’s top 30 most expensive and affordable rental suburbs for each capital city as well as all key rent and yield statistics.

Vaucluse in Sydney’s eastern suburbs is Australia’s most expensive suburb for house rentals, with a median weekly rental value of $2,308 compared to Elizabeth South in Adelaide, where tenants pay a median rent of $317 per week.

For units, Sydney’s Point Piper, also in the city’s eastern suburbs, has the most expensive rent at $1086 per week compared to Orelia, almost 40km south of Perth, which has the country’s most affordable median unit rents at $258 per week.

ALSO READ: Rentvesting – Paving the way to prosperity

[ad_2]

Source link